Introduction

Just got your first job? Earning around ₹25,000 per month? Congratulations! But now comes the real challenge—managing that salary without letting it disappear before the month ends.

If you’re between 20-25 years old, this is the perfect time to build smart money habits. The good news? You don’t need to be a finance expert. This guide breaks down everything in simple language—no confusing terms, just practical advice you can use today.

In this guide, you’ll learn:

- How to split your ₹25,000 salary smartly

- Where to save (and how much)

- Simple investment options that actually work

- How to enjoy life without going broke

- Common money mistakes to avoid

Let’s dive in!

Why Money Management Matters in Your 20s

Your 20s are like planting seeds for your future. The money habits you build now will either help you or haunt you later.

Here’s what happens if you manage money well:

- You’ll have emergency cash when your laptop dies or medical bills arrive

- You can afford that trip to Goa without asking parents for money

- You’ll start building wealth early (even small amounts grow big over time)

- Less stress about paying rent or credit card bills

Related: Emergency Fund vs Savings Account: 7 Critical Differences – Learn why keeping emergency money separate is crucial for financial security.

Here’s what happens if you don’t:

- Living paycheck to paycheck (constantly broke before month-end)

- Borrowing from friends repeatedly

- Missing out on opportunities because you have no savings

- Starting your 30s with debt instead of wealth

The choice is yours. Let’s make it a smart one.

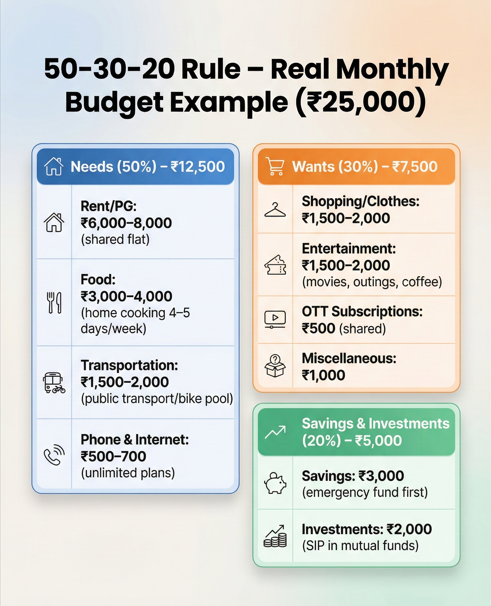

The 50-30-20 Rule: Your Money Split Formula

This is the simplest way to divide your ₹25,000 salary. No calculator needed!

50% – Needs (₹12,500)

Money you MUST spend to survive:

- Rent or PG accommodation

- Groceries and meals

- Transportation (petrol, metro, auto)

- Mobile recharge and internet

- Electricity bill (if applicable)

30% – Wants (₹7,500)

Things that make life enjoyable but aren’t essential:

- Eating out with friends

- Movies, OTT subscriptions (Netflix, Prime)

- Shopping (clothes, gadgets)

- Hobbies and entertainment

- Weekend trips

20% – Savings & Investments (₹5,000)

Money for your future:

- Emergency fund

- Investments (mutual funds, fixed deposits)

- Insurance

- Long-term goals

Pro Tip: If your rent is too high and you can’t stick to 50%, adjust to 60-25-15. The key is to ALWAYS save at least 15-20%.

Your Practical ₹25,000 Monthly Budget Plan

Let me show you a real example:

| Category | Amount | Details |

|---|---|---|

| Rent/PG | ₹6,000-8,000 | Share a flat to save money |

| Food | ₹3,000-4,000 | Cook at home 4-5 days/week |

| Transportation | ₹1,500-2,000 | Use public transport, bike pool |

| Phone/Internet | ₹500-700 | Choose unlimited plans |

| Shopping/Clothes | ₹1,500-2,000 | Buy only when needed |

| Entertainment | ₹1,500-2,000 | Movies, outings, coffee |

| OTT Subscriptions | ₹500 | Share with friends |

| Miscellaneous | ₹1,000 | Unexpected small expenses |

| Savings | ₹3,000 | Emergency fund first |

| Investments | ₹2,000 | SIP in mutual funds |

| Total | ₹25,000 |

Adjust this based on your city: Living in Mumbai or Bangalore costs more than Pune or Jaipur. If rent is higher, cut entertainment slightly but NEVER skip savings.

Step-by-Step: How to Start Managing Money Today

Step 1: Track Where Your Money Goes (Week 1)

For 7 days, write down EVERY rupee you spend. Use a simple notebook or free apps like:

- Walnut – Download from Google Play Store

- Money Manager – Download from Google Play Store

- Even Google Sheets works

You’ll be shocked to see how much you waste on unnecessary things like daily chai-samosa (₹50 × 30 days = ₹1,500/month!).

Step 2: Open a Separate Savings Account

Have two bank accounts:

- Salary Account – Where money comes in

- Savings Account – Where you transfer ₹5,000 immediately after salary

Why? Because “out of sight, out of mind.” If money stays in your main account, you’ll spend it.

Step 3: Set Up Automatic Savings

Most banks allow automatic transfers. Set up:

- ₹3,000 → Savings account on salary day

- ₹2,000 → Investment (SIP in mutual fund)

This happens automatically. You won’t even see this money, so you won’t miss it.

Step 4: Build Your Emergency Fund First

Before investing anywhere, save ₹15,000-30,000 as emergency money. This is for:

- Sudden medical expenses

- Job loss (very rare, but better safe)

- Urgent family needs

- Laptop/phone damage

Keep this in a regular savings account or sweep account where you can access it instantly.

Must Read: How Much Should You Keep in Emergency Fund? Complete Guide for Indians – Calculate your exact emergency fund amount based on lifestyle.

Target: Save ₹3,000/month = ₹18,000 in 6 months

Step 5: Start Small Investments

Once you have an emergency fund, start investing ₹2,000/month. Best options for beginners:

Option 1: Mutual Fund SIP (Recommended)

- Start with index funds like Nifty 50 or Sensex funds

- Use apps like Groww, Zerodha Coin, or Paytm Money

- Invest ₹1,000-2,000 monthly

- Long-term returns: 12-15% per year (better than FD)

Learn More: Mutual Funds for Beginners: Complete SIP Guide 2026 – Step-by-step tutorial on starting your first SIP investment.

Option 2: Public Provident Fund (PPF)

- Minimum ₹500, maximum ₹1.5 lakh per year

- 7.1% interest (tax-free) – Check latest PPF rates on India Post

- Lock-in period: 15 years (good for long-term)

Option 3: Recurring Deposit (RD)

- Safe option for beginners

- 6-7% interest

- Can withdraw after 1-5 years

Pro Tip: Start with 50% in mutual funds and 50% in RD/PPF. As you learn more, increase mutual fund percentage.

Smart Saving Tips for ₹25,000 Salary

1. Cook at Home 4-5 Days a Week

Eating out every day costs ₹150-200 = ₹6,000/month. Cooking at home costs ₹3,000-4,000. You save ₹2,000-3,000!

2. Use Public Transport

If you’re spending ₹5,000/month on Ola/Uber, switch to metro or bus. Save ₹3,000 easily.

3. Share Subscriptions

Netflix, Prime, Spotify – share with 3-4 friends. Your ₹800 cost becomes ₹200.

4. Buy Clothes in Sales

Wait for end-of-season sales. Buy 3 shirts for the price of 1.

5. Avoid Small Daily Expenses

That daily ₹50 chai-samosa = ₹1,500/month. Make tea at home, carry snacks.

6. Use Credit Cards Wisely (or Avoid Them)

If you have a credit card:

- ALWAYS pay full amount before due date

- Never pay just “minimum amount due”

- Use it only for big purchases (not daily chai)

Related Guide: Credit Card vs Debit Card: Which Is Better for Young Indians? – Understand the pros and cons before getting your first credit card.

Better option: Use debit card. You can only spend what you have.

7. Find a Side Hustle

Earn extra ₹3,000-5,000/month:

- Freelance writing, design, coding on Fiverr or Upwork

- Tutoring students online via Chegg or Vedantu

- Selling on Instagram/Meesho

- Part-time weekend gigs

Popular Article: 15 Side Hustles That Pay ₹5,000+ Monthly for Indian Students & Working Professionals – Complete guide with earning potential.

Extra income = More savings OR more fun money without guilt.

Common Money Mistakes to Avoid

Mistake 1: “I’ll Start Saving Next Month”

Next month never comes. Start TODAY with even ₹500.

Mistake 2: Buying Everything on EMI

That ₹30,000 phone on EMI feels cheap at ₹2,500/month. But you pay ₹3,000 extra in interest! Buy second-hand or wait and save.

Mistake 3: No Emergency Fund

Medical emergency + no savings = borrowing at high interest. Always keep ₹15,000-30,000 accessible.

Mistake 4: Following “Fake Rich” Lifestyle

Your friend earning ₹25,000 shows off new iPhone? He’s probably in debt. Don’t compare. Build YOUR wealth quietly.

Mistake 5: Ignoring Small Expenses

₹50 here, ₹100 there adds up to ₹3,000-4,000/month. Track everything.

Mistake 6: Not Learning About Money

Spend 15 minutes daily learning. Watch YouTube channels like:

External Resource: Investopedia’s Personal Finance Basics – Free financial education from trusted source.

Mistake 7: Keeping All Money in Savings Account

Savings account gives 3-4% interest. Inflation is 6-7%. You’re actually LOSING money. Invest smartly.

Your 6-Month Money Management Action Plan

Month 1-2: Foundation

- Track all expenses

- Open separate savings account

- Save ₹3,000/month minimum

- Cut unnecessary expenses

Month 3-4: Emergency Fund

- Continue saving ₹3,000/month

- Build emergency fund to ₹15,000

- Learn about mutual funds (watch videos)

Month 5-6: Start Investing

- Emergency fund complete

- Start SIP with ₹1,000-2,000/month

- Increase savings to ₹5,000/month if possible

After 6 months, you’ll have:

- ₹15,000 emergency fund

- ₹6,000-12,000 invested

- Smart money habits for life

FAQs: Money Management for Young Indians

Q1: I earn ₹25,000 but rent is ₹10,000. Can I still save?

Yes! Adjust to 60-25-15 rule. Share flat to reduce rent. Save at least ₹3,000/month.

Q2: Should I invest or clear small debts first?

ALWAYS clear debts first. Debt interest (15-20%) is higher than investment returns (12-15%).

Q3: Is mutual fund safe for beginners?

Index funds are relatively safe. Start small (₹1,000/month), invest for 5+ years. Don’t panic during market falls.

Expert Advice: SEBI’s Investor Education Portal – Learn about safe investing practices from India’s market regulator.

Q4: Can I save for both marriage and investment?

Yes! Split your ₹5,000 savings: ₹2,500 in RD for marriage (3-5 years), ₹2,500 in mutual funds for long-term.

Q5: Should I take health insurance at 23?

YES! Basic health insurance costs ₹400-500/month. One hospitalization without insurance can wipe out your savings.

Insurance Guide: PolicyBazaar’s Health Insurance Basics – Compare and buy affordable health insurance plans.

Q6: How do I handle family financial pressure?

Set boundaries. Help family, but keep 20% salary for yourself. Your future matters too.

Q7: Is buying insurance investment?

No! Insurance (term life, health) is protection, not investment. Keep them separate.

Final Thoughts: Your Money, Your Future

Managing ₹25,000 might seem tough, but thousands of young Indians are doing it successfully. The secret? Start small, stay consistent, and never stop learning.

Remember:

- Every ₹1,000 saved today becomes ₹2,000-3,000 in 5-7 years

- Your 20s are the BEST time to build wealth (thanks to compound interest)

- Small habits create big results

Action Step for Today: Don’t just read this article. Pick ONE thing from this guide and do it today:

- Download a money tracking app

- Open a separate savings account

- Start a ₹500 SIP in mutual fund

- Cut one unnecessary expense

Your future self will thank you!

Share Your Journey

Managing money at ₹25,000 salary? What’s your biggest challenge? Share in the comments below! Let’s learn from each other.

Found this helpful? Share with friends who need this!