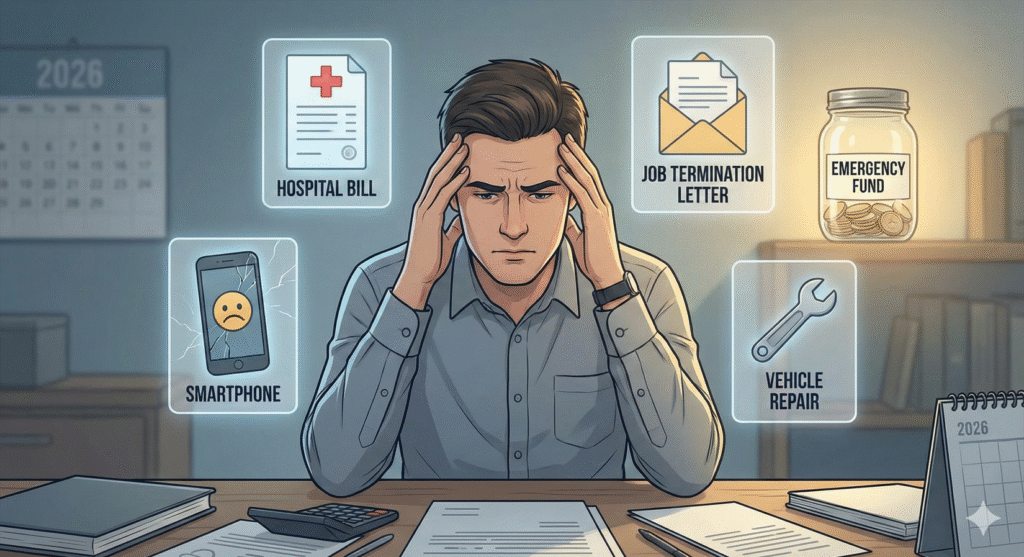

Imagine this: You wake up one morning to find your car has broken down, and the repair will cost ₹30,000. Or worse, you lose your job unexpectedly. Do you have enough money set aside to handle these situations without panicking or borrowing from family and friends?

If the answer is no, you need an emergency fund. In 2026, with economic uncertainties, rising inflation, and unpredictable job markets, having an emergency fund is not just a good idea—it’s essential for your financial security.

In this comprehensive guide, you’ll learn exactly how to build an emergency fund from scratch, how much you need, where to keep it, and the smartest strategies to reach your goal faster. Whether you’re earning ₹20,000 or ₹2 lakh per month, this guide will help you create a financial safety net.

What is an Emergency Fund?

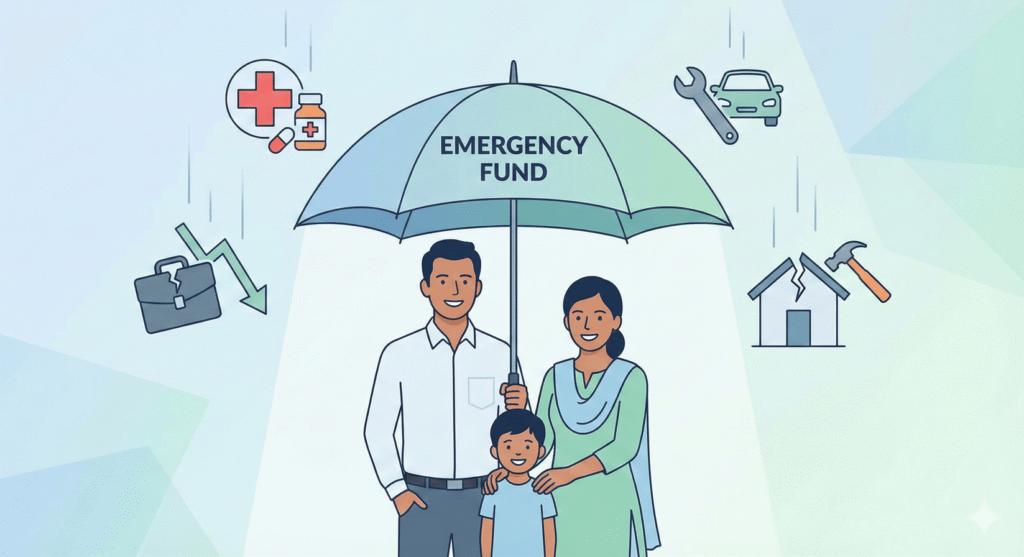

An emergency fund is money you set aside specifically for unexpected expenses or financial emergencies. Think of it as your financial safety net that catches you when life throws curveballs.

This is different from your regular savings account. Your savings might be for a vacation, a new phone, or a down payment on a house. Your emergency fund, however, is strictly for genuine emergencies like:

- Medical emergencies: Sudden hospitalization, surgery, or treatment not covered by insurance

- Job loss: Losing your job unexpectedly and needing money to survive until you find new employment

- Urgent home repairs: Water leakage, electrical issues, or structural damage that needs immediate fixing

- Vehicle breakdown: Major car or bike repairs that you need for daily commuting

- Family emergencies: Helping a family member in genuine crisis

The key word here is “emergency.” Notably, a shopping sale, a vacation, or buying the latest smartphone does NOT count as an emergency. According to Moneycontrol’s personal finance guide, distinguishing between wants and needs is crucial for financial discipline..

Why You Need an Emergency Fund in 2026

Protection Against Job Market Uncertainty

The job market in 2026 is more unpredictable than ever. With artificial intelligence changing industries, companies restructuring, and economic fluctuations, job security is no longer guaranteed. Even if you’re in a stable position today, circumstances can change overnight.

Having an emergency fund means that if you lose your job, you have enough money to cover your expenses for several months while you search for new opportunities. This removes the pressure of accepting the first job offer out of desperation, allowing you to make better career decisions.

Rising Medical Costs in India

Healthcare costs in India have been rising steadily at about eight to ten percent annually. Even if you have health insurance, there are often gaps in coverage—co-payments, room rent limits, certain procedures not covered, or waiting periods for specific illnesses. According to the Economic Times healthcare report, out-of-pocket medical expenses remain a major concern for Indian families.

An emergency fund ensures that you or your family members can get the medical care you need without worrying about immediate finances. Medical emergencies don’t wait for your next salary, and having funds readily available can literally be life-saving.

Peace of Mind and Financial Freedom

Beyond the practical benefits, an emergency fund provides something invaluable: peace of mind. When you know you have money set aside for emergencies, you sleep better at night. You’re not constantly worried about what will happen if something goes wrong.

This financial cushion also protects your relationships. You won’t need to borrow from family or friends, which can create uncomfortable situations and strain relationships. You won’t need to use high-interest credit cards or personal loans, which can trap you in a cycle of debt.

Financial freedom starts with having an emergency fund. It’s the foundation upon which all other financial goals are built.

How Much Should Your Emergency Fund Be?

The golden rule for emergency funds is to save three to six months’ worth of expenses. But the exact amount depends on your personal situation.

The 3-6 Month Rule Explained

Save 3 months of expenses if:

- You’re single with no dependents

- You have a stable job in a secure industry

- You have family support nearby

- You have good health insurance coverage

Save 6 months of expenses if:

- You’re married or have children

- You’re the sole earning member of your family

- You work in an industry with high job turnover

- You have ongoing health issues or family members who might need care

Save 9-12 months of expenses if:

- You’re self-employed or a freelancer

- You run your own business

- You work in a highly volatile industry

- You’re the only earning member with multiple dependents

Calculate Your Monthly Expenses

To determine your target emergency fund amount, first calculate your essential monthly expenses. Here’s an example:

Monthly Expenses Breakdown:

- Rent/Home EMI: ₹10,000

- Groceries and household items: ₹5,000

- Utilities (electricity, water, gas, internet): ₹2,000

- Loan EMIs (car, personal): ₹8,000

- Insurance premiums: ₹1,500

- Transportation (fuel, public transport): ₹3,000

- Children’s school fees: ₹4,000

- Miscellaneous essentials: ₹2,500

Total Monthly Expenses: ₹36,000

If you’re targeting 6 months, your emergency fund goal would be: ₹36,000 × 6 = ₹2,16,000

Notice that we’re only counting essential expenses. You don’t need to include money for dining out, entertainment, subscriptions, or shopping in your emergency fund calculation. In a genuine emergency, you’ll cut these expenses first.

Action Step: Take 10 minutes right now to list your monthly essential expenses. Importantly, be honest and realistic. This is your starting point. For more budgeting tips, check out our monthly budget planning guide (internal link to your budgeting article).

Step-by-Step Guide to Build Your Emergency Fund

Building an emergency fund might seem overwhelming, especially if you need to save over ₹2 lakh. But remember, this isn’t a sprint—it’s a marathon. Let’s break it down into manageable steps.

Step 1: Set a Realistic Target

Don’t try to save six months of expenses immediately. This approach often leads to frustration and giving up. Instead, break your goal into smaller milestones:

Milestone 1: Save ₹10,000 (your first mini emergency fund) Milestone 2: Save ₹25,000 (one month’s expenses) Milestone 3: Save ₹75,000 (three months’ expenses) Milestone 4: Save ₹1,50,000 (full six months’ expenses)

Celebrate each milestone. When you reach ₹10,000, you’ve already achieved something significant—you have money to handle small emergencies without going into debt.

Step 2: Open a Separate Savings Account

This is crucial. Do not keep your emergency fund in the same account as your regular spending money. Why? Because mental accounting matters.

When your emergency fund is mixed with your regular money, it’s too easy to dip into it for non-emergencies. “I’ll just take ₹5,000 for this sale and put it back next month” turns into a habit, and before you know it, your emergency fund is gone.

Best savings accounts for emergency funds in India:

- Look for accounts with high interest rates (currently between 4-7% for regular savings accounts)

- Zero or low minimum balance requirements

- Easy online and mobile banking access for emergencies

- No charges for withdrawals

Some good options include digital banks like DBS DigiBank, IDFC First Bank, or AU Small Finance Bank, which offer higher interest rates than traditional banks. However, choose a bank that you’re comfortable with and that has good customer service. For detailed reviews, visit BankBazaar’s comparison tool.

Step 3: Automate Your Savings

Automation is the secret weapon of successful savers. Set up an automatic transfer from your salary account to your emergency fund account on the day you receive your salary.

Why salary day? Because if you wait until the end of the month to save “whatever is left,” there will be nothing left. Pay yourself first.

How much to save automatically:

- If you earn ₹30,000/month: Start with ₹3,000-6,000 (10-20%)

- If you earn ₹50,000/month: Start with ₹5,000-10,000 (10-20%)

- If you earn ₹1,00,000/month: Start with ₹10,000-20,000 (10-20%)

Start with what’s comfortable. Even ₹1,000 per month is better than nothing. As you get used to living on less, gradually increase the amount.

Many banking apps and UPI apps like Google Pay, PhonePe, and Paytm allow you to set up recurring payments or automatic savings. Use these features to make saving effortless.

Step 4: Cut Unnecessary Expenses

This step is where most people can find significant money for their emergency fund without feeling deprived. Look for expenses that don’t add much value to your life.

Common areas to cut:

Subscriptions: Do you really watch all five OTT platforms? Cancel the ones you rarely use. Savings: ₹500-1,500/month

Dining out: Reduce eating out from 4 times a week to once a week. Cook at home more often. Savings: ₹3,000-5,000/month

Coffee and snacks: That daily ₹150 coffee adds up to ₹4,500/month. Make coffee at home or reduce to twice a week. Savings: ₹3,000/month

Unused gym membership: If you haven’t gone in months, cancel it. Exercise at home or outdoors. Savings: ₹1,000-2,000/month

Impulse shopping: Wait 48 hours before buying non-essential items. Most of the time, the urge will pass. Savings: ₹2,000-5,000/month

Brand products: Switch to generic or store brands for everyday items. The quality is often similar. Savings: ₹1,000-2,000/month

With these cuts alone, you could save ₹10,000-15,000 per month without drastically changing your lifestyle. For more money-saving strategies, read our guide to reduce monthly expenses (internal link).

Step 5: Use Windfalls Wisely

Windfalls are unexpected money that comes your way—bonuses, tax refunds, gifts, festival money from relatives, or income tax returns. These are golden opportunities to boost your emergency fund.

The 50-50 rule for windfalls: Put 50% into your emergency fund and use 50% for whatever you want—treat yourself, buy something you’ve been wanting, or invest in other goals.

Example: You receive a ₹40,000 bonus at work.

- ₹20,000 goes directly to your emergency fund

- ₹20,000 is yours to enjoy

This approach keeps you motivated while still making significant progress on your emergency fund. If you’re highly motivated or your emergency fund is severely lacking, consider the 80-20 rule instead—80% to emergency fund, 20% for yourself.

Step 6: Track Your Progress

What gets measured gets managed. Track your emergency fund progress regularly—at least once a month.

Ways to track:

- Use money management apps like Money Manager, Walnut, or ET Money

- Create a simple Excel spreadsheet

- Use a visual tracker (like a thermometer chart) on your wall

- Set reminders in your phone calendar to check your balance

Celebrate milestones. When you hit ₹25,000, treat yourself to something small. When you reach ₹1 lakh, celebrate with family. These celebrations reinforce positive behavior and keep you motivated for the long haul.

Pro tip: Share your goal with someone you trust—a spouse, close friend, or family member. Having an accountability partner increases your chances of success significantly.

Where to Keep Your Emergency Fund in 2026

Your emergency fund needs to be easily accessible (liquid) and safe. You don’t want to put it in investments where you might lose money or have to wait weeks to access it. Here are your best options:

Savings Bank Account

Pros:

- Immediate access to money

- No risk of losing principal

- DICGC insurance covers up to ₹5 lakh per bank

- Earns some interest (2.5-4% typically)

Cons:

- Relatively low interest rates

- Interest doesn’t keep pace with inflation

Best for: Your first ₹50,000-₹1,00,000 of emergency fund. Keep this amount in a regular savings account for instant access.

High-Yield Savings Account

Some banks offer savings accounts with interest rates of 6-7%, significantly higher than regular accounts. These are perfect for emergency funds.

Examples:

- DBS DigiSavings (up to 7% on balances up to ₹1 lakh)

- IDFC First Bank (6-7% depending on balance)

- AU Small Finance Bank (up to 7.25%)

Important: Check the terms carefully. Some high-yield accounts have conditions like minimum balance requirements, limited transactions, or interest rate slabs.

Best for: The bulk of your emergency fund (₹1 lakh to ₹3 lakh).

Liquid Mutual Funds

Liquid funds are debt mutual funds that invest in very short-term debt instruments. They typically offer returns of 4-6% annually and allow withdrawal within 24 hours (money credited to your account the next working day).

Pros:

- Higher returns than savings accounts

- Relatively safe (though not risk-free)

- Instant redemption facility available for up to ₹50,000

- No exit load (no penalty for withdrawal)

Cons:

- Not as instant as a savings account (24-hour delay)

- Minimal market risk (very rare, but possible)

- Requires KYC and some paperwork

Recommended liquid funds:

- HDFC Liquid Fund

- ICICI Prudential Liquid Fund

- Aditya Birla Sun Life Liquid Fund

Best for: The portion of your emergency fund above ₹3 lakh, once you have good coverage in savings accounts.

Fixed Deposits with Premature Withdrawal

Short-term FDs (6-12 months) can work for part of your emergency fund, but with caution.

Pros:

- Guaranteed returns (5-7%)

- Safe and insured up to ₹5 lakh

Cons:

- Penalty for premature withdrawal (usually 0.5-1% less interest)

- Takes 1-2 days to break FD and get money

- Some banks charge processing fees

Best for: A small portion of your emergency fund (maybe 20-30%) if you already have adequate liquid funds

Where NOT to Keep Your Emergency Fund

Stock Market/Equity Mutual Funds: Too volatile. Your ₹2 lakh emergency fund could become ₹1.5 lakh right when you need it.

Real Estate: Completely illiquid. Can’t sell a property in an emergency.

Long-term Fixed Deposits: Heavy penalties and delays in breaking them.

PPF or ELSS Funds: Locked-in for years; not accessible in emergencies.

Cryptocurrency: Extremely volatile and risky for emergency funds.

The ideal distribution for a ₹2 lakh emergency fund:

- ₹50,000 in regular savings account (instant access)

- ₹1,00,000 in high-yield savings account

- ₹50,000 in liquid mutual funds

This gives you layered liquidity—some money instantly available, some within 24 hours, all while earning decent returns.

Common Mistakes to Avoid

Mistake 1: Using Emergency Fund for Non-Emergencies

The biggest mistake people make is dipping into their emergency fund for things that aren’t genuine emergencies.

Not an emergency:

- Buying things on sale (“But I’m saving 50%!”)

- Vacation (“We really need a break”)

- Latest smartphone or gadget

- Festival shopping

- Lending money to friends

Genuine emergencies:

- Medical emergency

- Job loss

- Critical home repairs (water damage, electrical issues)

- Vehicle breakdown affecting your livelihood

- Family crisis requiring immediate travel

Before using your emergency fund, ask: “Is this truly urgent and unexpected? Will waiting cause serious harm?” If you can wait, save, or postpone, it’s not an emergency.

Mistake 2: Investing in Risky Assets

Some people think, “Why should my emergency fund earn only 4-5%? I can get 12-15% in stocks!” This is a dangerous approach.

Your emergency fund is not for growing wealth—it’s for protection. Safety and liquidity are more important than returns. The worst possible scenario is needing your emergency fund during a market crash and finding it’s lost 30% of its value.

Mistake 3: Not Replenishing After Use

If you use your emergency fund, that’s exactly what it’s there for—don’t feel guilty. But the key is to rebuild it immediately.

Let’s say you have ₹2 lakh in your emergency fund and you use ₹40,000 for a medical emergency. Your new priority should be getting that ₹40,000 back as quickly as possible. Increase your monthly savings temporarily, use your next bonus, or cut extra expenses until you’re back to your full emergency fund amount.

Mistake 4: Keeping Too Much

Yes, you can have too much in your emergency fund. If you have 18 months or 2 years of expenses sitting in a savings account, that’s excessive. Money beyond 12 months of expenses should be invested for other goals like retirement, children’s education, or wealth building.

Emergency funds are meant to protect you, not to sit idle indefinitely. Once you’ve reached your target (3-6 months of expenses), redirect your savings to other financial goals and investments that offer better returns.

Emergency Fund vs Other Financial Goals

Many people wonder: “Should I build my emergency fund first, or should I invest for retirement? Should I pay off debt first?” Here’s a clear priority framework:

Financial Priority Pyramid:

Level 1: Basic Emergency Fund (₹25,000-50,000) Before anything else, get at least ₹25,000-50,000 set aside. This prevents you from going into debt for small emergencies.

Level 2: Pay Off High-Interest Debt If you have credit card debt (36-42% interest) or personal loans (14-18% interest), aggressively pay these off. These interest rates are killing your finances.

Level 3: Complete Emergency Fund (3-6 months expenses) Now focus on building your full emergency fund. This is your financial foundation.

Level 4: Get Adequate Insurance Health insurance and term life insurance (if you have dependents) should be in place. Insurance is your emergency fund’s best friend—it prevents some emergencies from becoming financial disasters.

Level 5: Retirement Planning & Investments Only after you have your emergency fund and insurance in place should you focus heavily on retirement savings and long-term investments.

Level 6: Other Goals House down payment, children’s education fund, vacation savings, etc.

The key is that levels 1-4 are about protection. Levels 5-6 are about growth and lifestyle. You can’t skip the protection part and jump to growth—that’s building a house on sand.

Tips for Low-Income Earners

“But I only earn ₹20,000-25,000 per month. After expenses, there’s barely anything left. How can I build an emergency fund?”

This is a valid concern, but it’s not impossible. Here’s how:

Start with ₹500 per Month

If ₹5,000 per month sounds impossible, start with ₹500. That’s about ₹17 per day. Can you save ₹17 per day? That’s one cup of chai from a café, or one auto ride, or skipping one samosa.

₹500 per month = ₹6,000 per year = ₹30,000 in 5 years

Is it slow? Yes. But it’s infinitely better than having zero emergency fund.

Increase Savings with Income Growth

Every time you get a salary increment, immediately increase your emergency fund contribution. If you get a ₹2,000 raise, add ₹1,000 to your monthly emergency fund savings. You were already living on your previous salary, so you won’t miss this money.

Use the Envelope Method

If digital savings don’t work for you, try the physical envelope method. Every day, put whatever small amount you can spare in an envelope—₹20, ₹50, ₹100. At the end of the month, deposit it into your emergency fund account.

Find Additional Income

Can you take on a small side gig? Tutoring, freelancing, selling handmade items, or weekend part-time work? Even an extra ₹3,000-5,000 per month dedicated entirely to your emergency fund can help you reach your goal much faster.

Reduce Your Target

Instead of 6 months of expenses, aim for 3 months initially. For someone earning ₹25,000 with ₹20,000 in expenses, 3 months would be ₹60,000 instead of ₹1,20,000. This feels more achievable and keeps you motivated.

Remember: The goal is not to compare yourself with someone earning ₹1 lakh per month. The goal is to have YOUR personal safety net, whatever that looks like for your situation.

Real-Life Success Stories

Rahul’s Story (Mumbai, Age 29, Software Engineer)

Rahul earned ₹45,000 per month but had never thought about emergency funds. He lived paycheck to paycheck, using his credit card whenever unexpected expenses came up.

In January 2024, he set a goal to save ₹2 lakh (6 months of expenses). He automated ₹5,000 per month into a separate savings account, cut his dining out expenses, and canceled two OTT subscriptions he rarely used.

By December 2024, he had ₹60,000 saved. Not quite his target, but when his company announced layoffs in January 2025, he wasn’t panicking like his colleagues. He used those 3 months to find a better job while his emergency fund covered his expenses. He’s now back on track to complete his ₹2 lakh goal.

Priya’s Story (Delhi, Age 35, Teacher)

Priya earned ₹35,000 per month and was a single mother. Her father suddenly needed bypass surgery, and even with insurance, the out-of-pocket expenses were ₹80,000.

She had to borrow from relatives and use her credit card, taking months to repay the debt. This experience taught her the importance of an emergency fund.

She started with just ₹2,000 per month, but consistently saved for 2 years. When her son had an accident requiring ₹45,000 in medical expenses, she had ₹48,000 in her emergency fund. She paid for it without borrowing a single rupee. She calls it the best financial decision of her life.

Amit’s Story (Pune, Age 42, Business Owner)

Amit ran a small manufacturing business with fluctuating income. In good months, he earned ₹1-1.5 lakh; in slow months, sometimes just ₹40,000.

He built a 12-month emergency fund of ₹6 lakh over 3 years. When the pandemic hit and his business had zero income for 4 months, his emergency fund kept his family afloat. His business recovered, and he replenished his fund. He now keeps 18 months of expenses saved because of the unpredictable nature of his income.

These stories show that emergency funds work, regardless of your income level or situation. The key is starting and being consistent.

Emergency Fund Checklist for 2026

Ready to start building your emergency fund? Use this checklist:

☐ Step 1: Calculate your monthly essential expenses (rent, food, utilities, EMIs, insurance, transportation)

☐ Step 2: Determine your target (3, 6, or 12 months of expenses based on your situation)

☐ Step 3: Set smaller milestones (₹10,000, ₹25,000, ₹50,000, etc.)

☐ Step 4: Open a separate savings account specifically for emergency fund

☐ Step 5: Set up automatic transfer from salary account on payday

☐ Step 6: Identify and cut 2-3 unnecessary expenses

☐ Step 7: Commit to putting 50% of all windfalls into emergency fund

☐ Step 8: Set up tracking system (app, spreadsheet, or notebook)

☐ Step 9: Review progress monthly and adjust as needed

☐ Step 10: Once goal is reached, maintain it by replenishing after any use

Print this checklist and stick it somewhere visible. Each time you complete a step or hit a milestone, check it off. Visual progress is incredibly motivating.

Frequently Asked Questions (FAQ)

Should I build emergency fund or pay off debt first?

This depends on the type of debt and interest rate:

Pay off first (before building full emergency fund):

- Credit card debt (35-42% interest)

- Personal loans with very high interest (above 18%)

Build mini emergency fund first (₹25,000-50,000), then pay off:

- Personal loans (12-16% interest)

- Car loans (8-12% interest)

Pay simultaneously:

- Home loans (8-10% interest) – these are low-interest, so you can build your emergency fund while making regular EMI payments

Why the mini emergency fund? Without it, any small emergency will force you back into debt, creating a vicious cycle. Get ₹25,000-50,000 saved first, then tackle high-interest debt aggressively, then complete your full emergency fund.

Can I use my credit card as an emergency fund?

No. This is a common misconception and a dangerous one. Here’s why:

- Credit cards charge 36-42% annual interest if you don’t pay the full balance

- Using credit in an emergency means you’re now in debt during a crisis

- Credit limits can be reduced or cards can be cancelled without notice

- Builds bad financial habits

Your credit card can be a backup to your emergency fund, but never the primary emergency fund. Ultimately, ₹2 lakh in actual savings is infinitely better than a ₹2 lakh credit limit.

How long does it take to build an emergency fund?

This varies based on your income and expenses:

- Saving ₹5,000/month: 12 months to reach ₹60,000, 24 months for ₹1.2 lakh

- Saving ₹10,000/month: 12 months to reach ₹1.2 lakh, 18 months for ₹1.8 lakh

- Saving ₹15,000/month: 12 months to reach ₹1.8 lakh, 16 months for ₹2.4 lakh

Most people take 12-24 months to build a full emergency fund of 3-6 months of expenses. This is normal and healthy—building wealth takes time. The important thing is to start and stay consistent.

What counts as an emergency?

Genuine emergencies:

- Unexpected medical expenses

- Job loss or significant income reduction

- Essential home repairs (plumbing burst, roof leak, electrical failure)

- Car breakdown that prevents you from getting to work

- Emergency travel for family crisis

- Urgent pet medical care (if you have pets)

NOT emergencies:

- Sales and discounts

- Vacation or holidays

- Festivals and celebrations

- New gadgets or electronics

- Home renovation or upgrades

- Investing opportunities

- Helping friends with their expenses

When in doubt, ask: “Is this unexpected? Is it urgent? Will delaying cause serious harm? Is there no other way to handle this?” If you answer no to any of these, it’s not an emergency.

Should I tell my family about my emergency fund?

This is a personal decision, but here are some guidelines:

Definitely tell:

- Your spouse/life partner – you’re a team, and they should know about all financial safety nets

- Adult children you’re financially responsible for (if relevant)

Consider telling:

- Parents or siblings if you live with them

- Anyone who might otherwise lend you money in an emergency

Don’t need to tell:

- Extended family members

- Friends and colleagues

- Distant relatives

Why keep it somewhat private? Because once people know you have money saved, they might ask for loans or expect you to help them financially. While helping family is important, your emergency fund is for YOUR emergencies, not for lending out.

However, being transparent with your immediate household about finances, including emergency funds, builds trust and ensures everyone is working toward the same goals.

I already have health insurance. Do I still need an emergency fund?

Absolutely yes. Health insurance is essential, but it doesn’t cover everything:

- Co-payments and deductibles you must pay

- Room rent limits (if your room costs more, you pay the difference)

- Waiting periods for certain conditions

- Disease-specific caps

- Pre and post-hospitalization expenses not covered

- Consumables that aren’t covered

- Treatment in non-network hospitals

Beyond medical emergencies, your insurance doesn’t help with job loss, home repairs, vehicle breakdowns, or other financial emergencies. Health insurance and emergency funds work together—they don’t replace each other.

What if I have irregular income (freelancer/business owner)?

If your income fluctuates, you need a LARGER emergency fund—typically 9-12 months of expenses instead of 3-6 months.

Additional strategies:

- Save aggressively during good income months

- Keep your emergency fund in high-yield savings so it at least keeps pace with inflation

- Separate your emergency fund from business expenses (have both personal and business emergency funds)

- Consider the lowest income month you’ve had in the past year as your baseline

Irregular income makes planning harder, but it also makes an emergency fund even more critical. Your emergency fund essentially becomes your salary during slow months.

Conclusion: Take Action Today – Start Your Emergency Fund Journey

Building an emergency fund is one of the most important financial decisions you’ll ever make. It’s the foundation of financial security, the buffer that protects you from life’s uncertainties, and the tool that gives you peace of mind.

Remember these key points:

- Start with a realistic goal—even ₹25,000 makes a difference

- Automate your savings so consistency is built into your system

- Keep your emergency fund separate and easily accessible

- Never use it for non-emergencies, no matter how tempting

- Replenish it immediately after use

You don’t need to save ₹2 lakh by next month. Additionally, depriving yourself of all pleasures isn’t necessary either. Simply start today—right now—with whatever amount you can afford.

Your action step for today: Open a separate savings account for your emergency fund. Even if you transfer just ₹100 to start, you’ve begun your journey. That’s ₹100 more than you had yesterday.

Financial security isn’t about being rich; it’s about being prepared. Your future self will thank you for starting this journey today.

Start with just ₹500 this month. You’ve got this.

Did you find this guide helpful? Share it with someone who needs to hear this. Building financial security together makes us all stronger.

Have questions about building your emergency fund? Drop a comment below, and let’s discuss your specific situation.