Are you confused about the difference between an emergency fund and a savings account? You’re not alone. Moreover, 73% of Indians use these terms interchangeably, which leads to serious financial mistakes. In this comprehensive guide, you’ll discover the 7 critical differences between emergency fund vs savings account and learn which one you should prioritize in 2026.

By the end of this article, you’ll know exactly where to keep your money, how much to save in each account, and the costly mistakes that could drain your finances. Additionally, we’ll cover real examples from Indian households to help you make the right financial decisions.

What is a Savings Account?

A savings account is a bank account where you deposit money that you’re saving for various goals, purchases, or future needs. Essentially, it’s a general-purpose account for accumulating money over time.

Common Uses of Savings Accounts:

- Saving for a vacation or holiday trip

- Building funds for a down payment on a house

- Accumulating money for a car purchase

- Saving for festival shopping (Diwali, weddings)

- Putting aside money for gadgets, electronics

- General purpose savings without specific urgency

- Money you’re actively growing for future goals

Key characteristic: Savings accounts are for planned expenses and goals. Furthermore, you know what you’re saving for and approximately when you’ll need the money.

What is an Emergency Fund?

An emergency fund is money specifically set aside for unexpected, urgent expenses that you cannot plan for. Consequently, it acts as your financial safety net when life throws curveballs.

Genuine Emergencies Include:

- Sudden job loss or income reduction

- Medical emergencies not covered by insurance

- Urgent home repairs (water leak, electrical issues)

- Vehicle breakdown affecting your commute

- Family emergencies requiring immediate travel

- Unexpected legal expenses

- Critical appliance replacement (refrigerator, water heater)

Key characteristic: Emergency funds are for unplanned, urgent situations. You don’t know when (or if) you’ll need to use this money, but when you do, you need it immediately. According to research by Economic Times, 68% of Indians have faced unexpected expenses in the past year, yet only 32% had adequate emergency savings.

Emergency Fund vs Savings Account: The 7 Critical Differences

Difference 1: Purpose and Intent

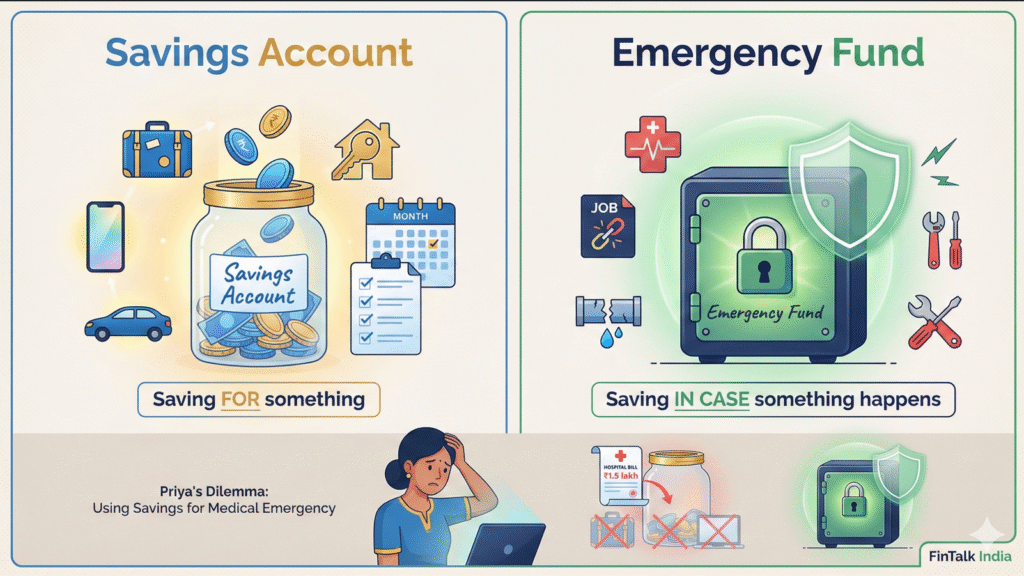

Savings Account:

- Purpose: Accumulate money for known goals

- Intent: Grow wealth for future planned purchases

- Mindset: “I’m saving FOR something”

- Examples: Vacation, new phone, car, house down payment

Emergency Fund:

- Purpose: Protection against unknown emergencies

- Intent: Financial safety net, not for growth

- Mindset: “I’m saving IN CASE something happens”

- Examples: Job loss, medical crisis, urgent repairs

Real Example: Priya from Mumbai had ₹2 lakh in her savings account, earmarked for a vacation and new laptop. When her father needed emergency surgery costing ₹1.5 lakh, she used her “savings.” Result? No vacation, no laptop, and months of guilt. If she had separated her emergency fund (₹1.5 lakh) from vacation savings (₹50,000), she could have handled the crisis without sacrificing her goals.

Key Takeaway: Your emergency fund protects your other financial goals. Without it, every emergency derails your savings plans. Learn more about how to build a proper emergency fund here

Difference 2: Accessibility Requirements

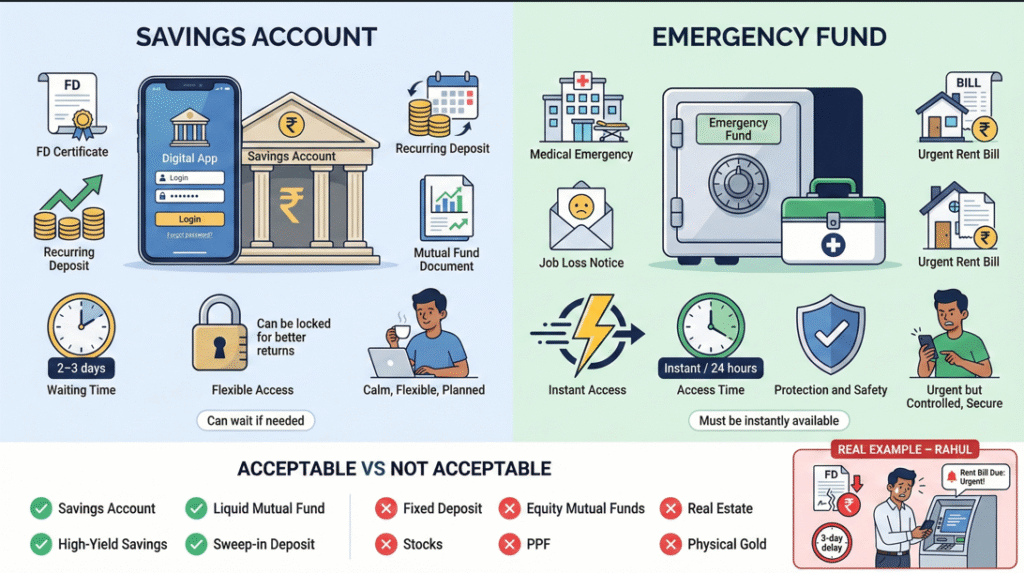

Savings Account:

- Accessibility: Can wait a few days if needed

- Acceptable options: FDs, recurring deposits, some mutual funds

- Liquidity: Medium to high

- Timeline: You control when to withdraw

- Can be: Locked for better returns (like FDs)

Emergency Fund:

- Accessibility: Must be instantly available

- Acceptable options: Only highly liquid accounts

- Liquidity: Extremely high (24-hour access maximum)

- Timeline: Emergencies don’t wait

- Cannot be: Locked, restricted, or hard to access

What “Instant Access” Really Means:

✅ Acceptable for Emergency Fund:

- Regular savings account (instant)

- High-yield savings account (instant)

- Liquid mutual funds (24-hour redemption)

- Sweep-in deposits (instant)

❌ NOT Acceptable for Emergency Fund:

- Fixed deposits (penalty + time delay)

- Equity mutual funds (volatile + 3-day settlement)

- Stocks (volatile + 2-day settlement)

- PPF (locked for years)

- Real estate (takes months to sell)

- Gold (need to sell physically)

Real Example: Rahul kept his emergency fund in a 5-year fixed deposit for higher interest (7.5% vs 4%). When he lost his job unexpectedly, he had to break the FD. Consequently, he paid a penalty, lost interest, and the bank took 3 days to process. Meanwhile, he couldn’t pay rent on time. Lesson learned: Accessibility trumps returns for emergency funds.

For detailed guidance on where to keep your emergency fund safely, read our complete guide on emergency fund storage options.

Difference 3: Ideal Amount to Keep

Savings Account:

- Amount: No fixed rule

- Depends on: Your goals and timeline

- Can be: ₹10,000 or ₹10 lakh depending on goals

- Growth focused: More is better

- Calculation: Based on what you’re saving for

Example Savings Goals:

- Vacation: ₹50,000

- New phone: ₹40,000

- Car down payment: ₹2,00,000

- Total in savings: ₹2,90,000

Emergency Fund:

- Amount: 3-6 months of expenses (specific formula)

- Depends on: Your monthly essential expenses

- Should be: ₹1.5-3 lakh for most Indian households

- Protection focused: Enough to survive emergencies

- Calculation: Monthly expenses × 6

How to Calculate Your Emergency Fund:

Step 1: List essential monthly expenses:

Rent/EMI: ₹12,000

Groceries: ₹6,000

Utilities: ₹2,500

Insurance: ₹2,000

Loan EMIs: ₹8,000

Transportation: ₹3,000

Children's fees: ₹5,000

Medicines: ₹1,500

Total: ₹40,000/monthStep 2: Multiply by 6 months.

₹40,000 × 6 = ₹2,40,000Step 3: This is your emergency fund target!

Important: Emergency fund is NOT unlimited. Once you reach 6-9 months of expenses, redirect additional savings to other goals or investments. Keeping 2 years of expenses in a low-return emergency fund is inefficient.

Note: For freelancers or business owners with irregular income, aim for 9-12 months of expenses instead of 6.

Difference 4: When and How to Use the Money

- Savings Account:

- When: According to your plan

- How: Withdraw for planned purchases

- Frequency: As needed for your goals

- Replacement: Not mandatory (goal completed)

- Emotion: Excitement (you’re buying what you saved for!)

When to Use Savings:

- You saved ₹50,000 for vacation → Time for trip → Use it!

- You saved ₹1 lakh for laptop → Found good deal → Use it!

- You saved ₹3 lakh for car down payment → Ready to buy → Use it!

Emergency Fund:

- When: Only for genuine unexpected emergencies

- How: Withdraw only when truly necessary

- Frequency: Hopefully never, but available when needed

- Replacement: Immediately replenish after use

- Emotion: Relief (crisis managed) + urgency (rebuild ASAP)

When to Use Emergency Fund:

- Job loss

- Medical emergency

- Critical home repair

- Vehicle breakdown (if needed for work)

- Family emergency

When NOT to Use Emergency Fund:

- Shopping sale (“50% off!”)

- Festival shopping

- Vacation

- Gadget upgrade

- Friend’s request for loan

- Investment opportunity

- “Good deal” on anything

The Replacement Rule:

If you use ₹30,000 from your ₹2 lakh emergency fund:

- Your emergency fund is now ₹1.7 lakh

- You’re vulnerable again

- Priority #1: Rebuild to ₹2 lakh immediately

- Increase monthly savings temporarily if needed

- Use bonuses/windfalls to replenish faster

Real Example: Neha had ₹1.5 lakh emergency fund. Her laptop broke (₹50,000 replacement). She thought, “This is urgent, I need it for work.” However, this wasn’t a true emergency—she could rent/borrow temporarily or buy refurbished. She used emergency fund anyway. Two months later, medical emergency (₹80,000). Now her fund was depleted. Moreover, she went into debt.

Lesson: Be strict about what qualifies as an “emergency.” When in doubt, ask: “Is this unexpected AND urgent AND unavoidable?” If not all three, it’s not an emergency.

Difference 5: Investment Strategy and Returns

Savings Account:

- Strategy: Can take moderate risk for higher returns

- Acceptable investments: Mutual funds, FDs, bonds, stocks

- Returns: 5-12% annually depending on risk

- Time horizon: Usually 1-5 years

- Goal: Growth of money

- Can fluctuate: Yes (stocks/MFs can go up/down)

Good Investment Options for Savings:

- Debt mutual funds (6-8% returns)

- Balanced mutual funds (8-10% returns)

- Fixed deposits (5-7% returns)

- Recurring deposits (5-6.5% returns)

- Short-duration funds (5-7% returns)

According to Moneycontrol’s investment guide, savings for goals 2-5 years away should aim for 7-9% returns through balanced allocation.

Emergency Fund:

- Strategy: Zero risk approach, safety first

- Acceptable investments: Only savings accounts, liquid funds

- Returns: 3-6% annually (secondary consideration)

- Time horizon: Indefinite (always available)

- Goal: Preservation and liquidity of money

- Cannot fluctuate: No (principal must be safe)

Good Options for Emergency Fund:

- High-yield savings account (4-7% returns)

- Regular savings account (3-4% returns)

- Liquid mutual funds (4-5% returns)

- Sweep-in FDs (5-6% returns, instant liquidity)

Why Returns Don’t Matter Much for Emergency Fund:

Imagine you have ₹2 lakh emergency fund:

- At 4% (savings account): Earns ₹8,000/year

- At 12% (equity fund): Could earn ₹24,000/year

- Difference: ₹16,000/year

Sounds good? But here’s the catch:

Scenario: Medical emergency, need ₹1 lakh immediately

- Savings account: Withdraw ₹1 lakh today ✅

- Equity fund: Market down 20%, your ₹1 lakh is now ₹80,000. You take ₹20,000 LOSS trying to chase ₹16,000 extra return ❌

Lesson: Emergency fund is insurance, not investment. Accept lower returns for peace of mind and guaranteed liquidity.

For better investment strategies for your long-term savings, explore our beginner’s investment guide for Indians.

Difference 6: Psychological and Emotional Aspect

Savings Account:

- Feeling: Positive and exciting

- Emotion: Hope, anticipation, progress

- Motivation: Clear goal you’re working toward

- Satisfaction: When you use it for planned purpose

- Thought process: “I’m building toward something good!”

Example Emotions:

- Watching vacation fund grow: Excitement

- Reaching car down payment goal: Pride

- Buying dream gadget with savings: Joy

Emergency Fund:

- Feeling: Security and peace of mind

- Emotion: Relief, safety, confidence

- Motivation: Fear of worst-case scenarios

- Satisfaction: When you DON’T need to use it

- Thought process: “I’m protected if something goes wrong!”

Example Emotions:

- Having ₹2 lakh emergency fund: Sleep peacefully

- Unexpected expense happens: Calm (not panic)

- Job security uncertain: Confidence (you’re covered)

The Peace of Mind Factor:

Without Emergency Fund:

- Constant financial anxiety

- Every unexpected bill = stress

- Job insecurity = panic

- One emergency = debt spiral

- Borrow from family/friends (awkward)

With Emergency Fund:

- Financial confidence

- Unexpected bills = annoying but manageable

- Job insecurity = concerning but survivable

- One emergency = handled without debt

- Independent, don’t need to borrow

Real Example: Two colleagues, Amit and Suresh, both earning ₹60,000/month:

Amit: No emergency fund, saves everything for house down payment

- Car breaks down: ₹40,000 needed

- Uses credit card (36% interest)

- Takes 8 months to pay off

- Stress, sleepless nights, fights with wife

- House down payment delayed by 1 year

Suresh: ₹2 lakh emergency fund + separate house savings

- Car breaks down: ₹40,000 needed

- Uses emergency fund

- Rebuilds fund in 4 months

- Minor inconvenience, no stress

- House down payment on track

Which life sounds better?

Difference 7: Account Management and Organization

Savings Account:

- Organization: Can be in main bank account

- Convenience: Easy access for planned withdrawals

- Multiple goals: Might have sub-accounts or separate accounts for different goals

- Tracking: Active monitoring (watching it grow!)

- Integration: Connected to regular banking (UPI, cards)

Organization Tips for Savings:

- Car fund: ₹50,000 in Savings Account 1

- Vacation fund: ₹30,000 in Savings Account 2

- Gadget fund: ₹20,000 in Savings Account 3

Or: Use single savings account but track separately in Excel/app

Emergency Fund:

- Organization: MUST be in separate account

- Convenience: Intentionally less convenient (reduces temptation)

- Single purpose: One account, one goal only

- Tracking: Passive monitoring (just ensure it’s there)

- Integration: Minimal integration – no debit card, no UPI

Why Separate Account is Crucial:

Problem with keeping emergency fund in regular account: “I have ₹1 lakh for emergencies in my savings account” (which also has salary, expenses, everything else)

What actually happens:

- Week 1: ₹1 lakh emergency fund + ₹20,000 spending money = ₹1.2 lakh total

- Week 2: Paid ₹15,000 bill, saw ₹1.05 lakh balance, felt safe

- Week 3: Bought ₹8,000 gadget, saw ₹97,000, “still close to ₹1 lakh”

- Week 4: More expenses, ₹88,000 left

- Month 2: Emergency fund is now ₹75,000 (but you don’t realize it)

- Real emergency: Only ₹75,000 available, not ₹1 lakh

Solution: Separate Account Strategy

Account 1: Primary Salary/Spending Account (Main Bank)

- Salary comes here

- All expenses from here

- UPI, debit card, everything linked

- Balance fluctuates constantly

Account 2: Emergency Fund Account (Different Bank)

- Only deposits, minimal withdrawals

- No debit card

- No UPI linked

- Not connected to regular banking

- Out of sight, out of mind

Setup Example:

- Primary: HDFC Bank (salary, expenses, spending)

- Emergency Fund: IDFC First Bank or DBS DigiSavings (separate, untouched)

Additional Benefits of Separate Account:

- Mental accounting (you KNOW it’s only for emergencies)

- Reduced temptation (extra steps to access = time to reconsider)

- Higher interest (often digital banks give better rates)

- Clear tracking (account balance = emergency fund amount)

- Goal visualization (watching THIS account grow to target)

Pro Tip: Keep emergency fund in a different bank than your primary bank. The physical and digital separation reinforces the psychological boundary.

Which Should You Build First: Emergency Fund or Savings?

This is the most common question, and the answer depends on your current financial situation. Here’s the exact framework:

Priority Framework:

Step 1: Mini Emergency Fund (₹25,000-50,000)

- Build this FIRST, before anything else

- Takes 3-6 months typically

- Protects you from small emergencies

- Prevents you going into debt for minor issues

Step 2: Pay Off High-Interest Debt

- Credit cards (36-42% interest)

- Personal loans above 18% interest

- Pay these aggressively

- Don’t invest while paying 40% interest on debt!

Step 3: Complete Emergency Fund (3-6 months expenses)

- Now build full emergency fund

- Takes 6-12 months typically

- Foundation of all financial planning

- Your priority before fancy investments

Step 4: Specific Savings Goals

- Now start saving for goals

- Vacation fund

- Gadget fund

- House down payment

- Car fund

Step 5: Investments for Growth

- Retirement savings

- Wealth building

- Long-term investments

Real-World Example:

Meera’s Situation (Age 28, ₹45,000/month salary):

- No emergency fund

- ₹80,000 credit card debt (38% interest)

- Wants to save for vacation (₹60,000)

- Wants to start SIP investments

Wrong Priority:

- Start ₹5,000 SIP for “long-term wealth” (earning maybe 12%)

- While paying 38% interest on credit card

- And having zero emergency protection

Correct Priority:

Why this order?

- Emergency fund prevents new debt

- Paying 38% debt is better ROI than 12% SIP

- Once debt-free, can save faster

- Stable foundation before growth investments

Common Mistakes: Emergency Fund vs Savings Account

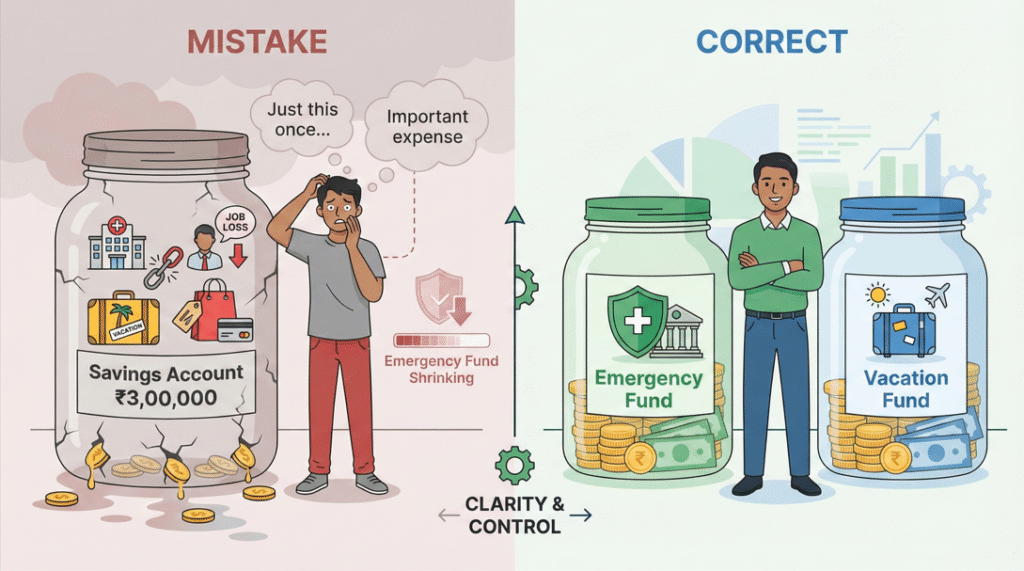

Mistake 1: Using Same Account for Both

The Problem: “I have ₹3 lakh in my savings account – ₹2 lakh for emergencies, ₹1 lakh for vacation.”

Why it fails:

- Money is fungible (all looks the same)

- Mental accounting breaks down

- You dip into “emergency” money for “important” things

- Emergency fund slowly depletes

- When real emergency comes, money isn’t there

Solution:

- Emergency fund: Separate account, different bank

- Vacation fund: Separate account or clearly tracked

- Never mix

Mistake 2: Keeping Emergency Fund in Low-Liquidity Options

The Problem: “My ₹2 lakh emergency fund is in a 5-year FD for 7.5% interest!”

Why it fails:

- Emergencies don’t wait for FD maturity

- Breaking FD = penalty + lost interest

- Takes 3-7 days to process

- You can’t pay hospital/rent/bills with “I have FD”

Real consequence: Rajesh had ₹3 lakh in FD as “emergency fund.” His daughter needed urgent surgery (₹1.5 lakh). Hospital wanted payment upfront. FD breaking took 5 days. He had to borrow from relatives at high interest for immediate payment. FD finally broke, he paid back relatives, but could have avoided the stress and interest cost.

Solution:

- Emergency fund = only highly liquid options

- Savings account (instant)

- Liquid funds (24 hours max)

- Accept 3-5% returns for liquidity

Mistake 3: No Emergency Fund Because “I Have Credit Card”

The Problem: “I don’t need emergency fund. I have ₹2 lakh credit card limit!”

Why it fails:

- Credit card = debt, not savings

- 36-42% interest if not paid

- During emergency, you’re adding debt stress

- Credit limits can be reduced without warning

- Card can be blocked/declined

- Using credit in crisis = financial hole deeper

Real Example: Vikram had no emergency fund but ₹3 lakh credit card limit. Lost job during pandemic. Used credit card for 3 months’ expenses (₹1.2 lakh). Took 6 months to find new job. By then, credit card bill was ₹1.5 lakh (with interest). Took 2 years to pay off. If he had emergency fund, no debt, no interest, no stress.

Truth: Credit card is a BACKUP to emergency fund, never a replacement.

Solution:

- Build emergency fund first

- Credit card is safety net #2

- Emergency fund = primary safety net

Mistake 4: Too Much in Emergency Fund

The Problem: “I have ₹8 lakh in emergency fund. I feel very safe!”

Why it’s inefficient:

- 6-9 months expenses = enough

- Beyond that = opportunity cost

- ₹8 lakh at 4% (savings) = ₹32,000/year

- ₹8 lakh at 12% (balanced fund) = ₹96,000/year

- You’re losing ₹64,000/year by over-saving in emergency fund

Sweet spot:

- 6 months expenses in emergency fund

- Rest in higher-return investments

- Balance safety with growth

Example: If your monthly expenses are ₹40,000:

- Emergency fund target: ₹2.4 lakh (6 months)

- If you have ₹5 lakh saved

- Keep ₹2.4 lakh in emergency fund

- Invest remaining ₹2.6 lakh in mutual funds/FDs for growth

Mistake 5: Not Replenishing After Use

The Problem: Used ₹50,000 from emergency fund for medical crisis. Emergency fund now ₹1.5 lakh instead of ₹2 lakh. Thinking “I’ll rebuild it eventually.” Never prioritizing it.

Why it fails:

- You’re vulnerable again

- Next emergency could hit anytime

- “Eventually” never comes

- Back to square one

Solution:

- Used emergency fund? Immediately make replenishment priority #1

- Increase monthly savings temporarily

- Use next bonus/windfall

- Get back to full amount ASAP

Timeline: Used ₹50,000 → Back to ₹2 lakh in 5 months max (save extra ₹10,000/month)

Mistake 6: Building Savings Before Emergency Fund

The Problem: “I’ll build emergency fund later. First, let me save for this vacation/gadget/car.”

Why it fails:

- Emergency can strike anytime

- You’re building on sand (no foundation)

- One emergency destroys all your savings progress

- Back to zero, plus possibly debt

Example: Pooja saved ₹1 lakh over 10 months for vacation (no emergency fund). Month 11: Car accident, ₹80,000 repair needed. Used vacation fund. No vacation, no emergency fund, back to zero after nearly a year of saving.

If she’d built ₹1 lakh emergency fund first, then saved for vacation:

- Car accident → Used emergency fund

- Vacation fund intact

- Rebuilt emergency fund over 8-10 months

- Eventually got vacation too

Solution:

- Emergency fund = foundation

- Build it fully before other goals

- Then save for wants

Comparison Table: Emergency Fund vs Savings Account

| Factor | Emergency Fund | Savings Account |

|---|---|---|

| Purpose | Unexpected emergencies only | Planned goals and purchases |

| Amount | 3-6 months of expenses (fixed formula) | Based on your goals (variable) |

| Accessibility | Must be instant (within 24 hours) | Can wait few days if needed |

| Where to Keep | Savings account, liquid funds only | Can be FDs, RDs, mutual funds |

| Returns Expected | 3-6% (not priority) | 5-12% (growth focused) |

| Risk Tolerance | Zero risk acceptable | Moderate risk okay |

| When to Use | Genuine emergencies only | When ready to achieve goal |

| After Use | Replenish immediately | Goal achieved, no replacement needed |

| Account Setup | Separate account (different bank) | Can be in main account |

| Emotional Role | Peace of mind, security | Excitement, anticipation |

| Priority | Build this FIRST | Build after emergency fund |

| Replacement | Mandatory after use | Not needed (goal achieved) |

Action Plan: How to Set Up Both Correctly

Step 1: Calculate Your Emergency Fund Target (15 minutes)

Worksheet:

Monthly Expenses:

Rent/EMI: ₹_______

Groceries: ₹_______

Utilities: ₹_______

Insurance: ₹_______

Loan EMIs: ₹_______

Transportation: ₹_______

Essential expenses: ₹_______

Other necessities: ₹_______

TOTAL per month: ₹_______

Multiply by 6: ₹_______ ← This is your emergency fund targetStep 2: Open Separate Emergency Fund Account (30 minutes)

Best Banks for Emergency Fund (High Interest + Good Service):

- IDFC First Bank (6-7% interest)

- DBS DigiBank (up to 7%)

- AU Small Finance Bank (up to 7.25%)

- RBL Bank (6-6.5%)

Setup Checklist:

- ☐ Open account online

- ☐ Don’t order debit card (or keep it locked away)

- ☐ Don’t link UPI

- ☐ Set up auto-transfer from salary account

- ☐ Label it “Emergency Fund Only” in app

Step 3: Start Automatic Transfers (5 minutes)

On Salary Day:

- ₹X → Emergency fund account (separate bank)

- ₹Y → Savings goal accounts

- Rest → Spending account

Example:

- ₹50,000 salary

- ₹10,000 → Emergency fund (IDFC Bank)

- ₹5,000 → Vacation savings (Same bank, different account)

- ₹35,000 → Main account (expenses)

Step 4: Track Progress (Monthly)

Simple Tracking:

Emergency Fund Goal: ₹2,40,000

Current Amount: ₹80,000

Remaining: ₹1,60,000

Saving per month: ₹10,000

Months to goal: 16 months

Target completion: May 2026For more detailed savings strategies, check our complete guide on how to save ₹1 lakh in 12 months.

Frequently Asked Questions

Can I use my emergency fund for a “good investment opportunity”?

Short answer: No.

Long answer: Investment opportunities come regularly. Real emergencies are rare but devastating. Using emergency fund for investments means:

- You’re no longer protected

- Opportunity cost of being unprotected is huge

- One emergency = debt spiral

- Emergency fund ≠ investment capital

If you have extra money beyond emergency fund, invest that. Don’t touch emergency fund.

Should I pay off loans or build emergency fund first?

Framework:

Pay loans first if:

- Interest rate above 18% (credit cards, high-interest personal loans)

- But keep mini emergency fund (₹25,000-50,000) first

Build emergency fund first if:

- Interest rate below 12% (home loans, education loans)

- These can continue while you build protection

Balance both if:

- Interest rate 12-18% (moderate personal loans)

- Build emergency fund while paying EMIs normally

Can I keep part of emergency fund in stocks/equity funds?

Short answer: No.

Long answer:

- Emergencies don’t wait for market recovery

- If market is down 30% when you need money = forced loss

- Emergency fund is insurance, not investment

- Keep 100% in safe, liquid options

After emergency fund is complete, invest extra money in stocks for growth.

How much should I have in savings vs emergency fund?

Formula:

Emergency Fund: 6 months expenses (₹2-3 lakh for most Indians)

Savings: Depends on your goals

- Short-term goals (under 1 year): Keep in savings account

- Medium-term goals (1-5 years): Can invest in debt funds, balanced funds

- Long-term goals (5+ years): Should be in equity investments

Example:

- Emergency fund: ₹2.4 lakh

- Vacation savings (6 months away): ₹40,000

- House down payment (3 years away): ₹5 lakh in balanced funds

- Retirement (30 years away): ₹2 lakh in equity mutual funds

My parents say emergency fund is unnecessary. Why do I need it?

Previous generations had:

- Lifetime job security (government jobs)

- Joint families (borrow from relatives easily)

- Lower medical costs

- Simpler lifestyle (fewer expenses)

Today’s reality:

- No job security (layoffs common)

- Nuclear families (can’t always ask relatives)

- High medical costs

- Higher living expenses

Plus: Having emergency fund = financial independence + dignity. Not borrowing from parents/relatives = adult responsibility.

Key Takeaways: Emergency Fund vs Savings Account

- Different purposes: Emergency fund = protection, Savings = goals

- Build emergency fund FIRST: Before investing or saving for wants

- Separate accounts mandatory: Don’t mix emergency fund with other money