Introduction

Personal finance management is the foundation of financial success and security. Whether you’re struggling with debt, trying to save for your first home, or planning for retirement, effective personal finance management can transform your financial future.

In today’s economy, where inflation and rising costs challenge everyone, mastering personal finance management isn’t optional—it’s essential. This comprehensive guide will teach you actionable strategies to budget smarter, save more, and build lasting wealth through proven personal finance management techniques.

According to a recent study by the Financial Planning Association, people who actively practice personal finance management are 3x more likely to achieve their financial goals. Let’s explore how you can join them.

What is Personal Finance Management?

Personal finance management is the process of planning, organizing, and controlling your financial activities. This includes budgeting, saving, investing, and managing debt to achieve your short-term and long-term financial goals.

Effective money management helps you build wealth, reduce financial stress, and create a secure future for yourself and your family.

Why Personal Finance Management Matters Now More Than Ever

The economic landscape of 2026 presents unique challenges and opportunities. With rising living costs, evolving employment patterns, and increasing financial complexity, mastering personal finance management has become essential for financial stability and growth.

People who actively manage their finances are better positioned to handle unexpected expenses, achieve major life goals, and build lasting wealth.

The 10 Pillars of Effective Personal Finance Management

1. Create a Realistic Budget (The Foundation of Personal Finance Management)

Budgeting is the cornerstone of personal finance management. A well-structured budget helps you understand where your money goes and ensures you’re allocating funds toward your priorities.

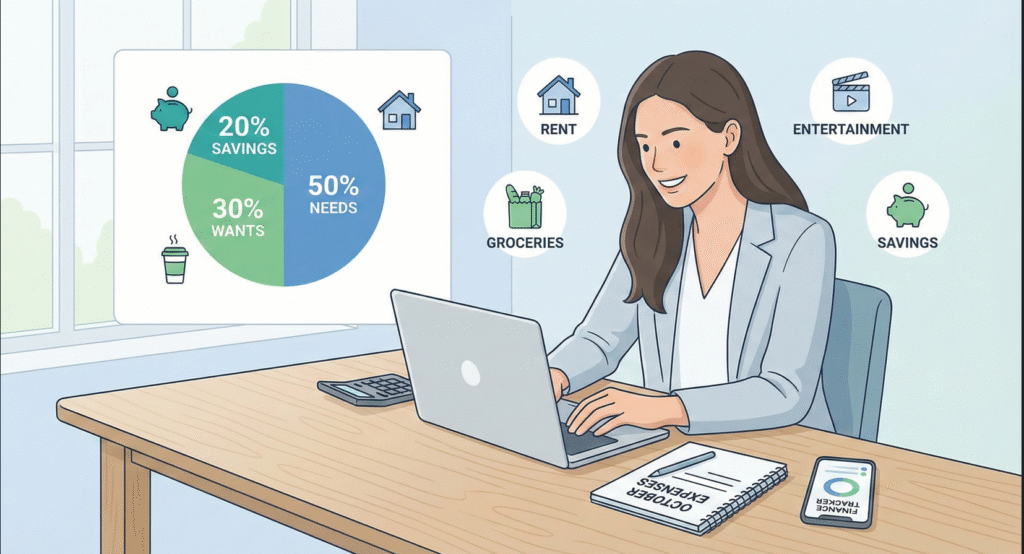

The 50/30/20 Budget Rule for Personal Finance Management:

This popular personal finance management framework divides your after-tax income into three categories: 50% for essential needs like housing and groceries, 30% for discretionary wants including entertainment, and 20% for savings and debt repayment.

Actionable Budgeting Tips:

- Track every expense for 30 days using apps like Mint or YNAB

- Categorize spending into fixed costs, variable costs, and discretionary spending

- Review your budget weekly for the first month, then monthly

- Use spreadsheet templates for manual tracking

- Automate bill payments to avoid late fees

Research from NerdWallet shows that people who budget save 15-20% more annually than those who don’t practice personal finance management.

2. Build Your Emergency Fund Through Personal Finance Management

An emergency fund is your financial safety net and a critical component of personal finance management. Financial experts recommend saving three to six months of living expenses.

How to Build Your Emergency Fund:

- Start with a mini-goal of $1,000 for beginners

- Automate transfers to a high-yield savings account like those offered by Marcus by Goldman Sachs or Ally Bank

- Save windfalls like tax refunds and bonuses

- Keep funds in accessible accounts, not invested in stocks

- Gradually increase to six months of expenses

According to Bankrate research, only 39% of Americans could cover a $1,000 emergency, highlighting why personal finance management skills are crucial.

3. Master Debt Management in Your Personal Finance Management Plan

Strategic debt management is essential for healthy personal finance management. Not all debt is equal—understanding repayment priorities can save thousands in interest.

Debt Repayment Strategies for Personal Finance Management:

The Debt Avalanche Method: Focus on high-interest debts first while making minimum payments on others. This personal finance management approach saves the most money on interest charges.

The Debt Snowball Method: Pay off smallest debts first for psychological wins that build momentum in your personal finance management journey.

Smart Debt Management Tips:

- Consolidate multiple high-interest debts through services like SoFi or LendingClub

- Negotiate lower interest rates with creditors

- Pay more than minimums whenever possible

- Use balance transfer cards strategically (0% APR offers)

- Avoid new debt while paying off existing balances

The Consumer Financial Protection Bureau offers free resources for debt management and personal finance management education.

4. Implement Smart Saving Strategies in Your Personal Finance Management

Consistent saving habits are the backbone of successful personal finance management. Building wealth requires disciplined saving across multiple goals.

Effective Savings Techniques:

- Pay yourself first by treating savings as a non-negotiable expense

- Use the “save more tomorrow” method—increase savings with each raise

- Open separate accounts for different goals using Ally Bank or Capital One 360

- Take advantage of employer retirement matching

- Automate everything possible

Recommended Savings Allocation for Personal Finance Management:

- Emergency fund: 3-6 months expenses

- Retirement: 15-20% of gross income

- Short-term goals: 5-10% of income

- Long-term goals: remaining discretionary income

Studies from Fidelity Investments show that automated savings increase wealth accumulation by 40% compared to manual saving.

5. Start Investment Planning for Long-Term Personal Finance Management

Investing transforms personal finance management from preservation to growth. Smart investing allows your money to work for you through compound interest and market appreciation.

Investment Basics for Personal Finance Management:

- Start with employer-sponsored 401(k) plans with matching

- Open an IRA through platforms like Vanguard or Fidelity

- Consider low-cost index funds for diversified exposure

- Understand your risk tolerance using tools from Charles Schwab

- Diversify across stocks, bonds, and real estate

Key Investment Principles:

- Start early to maximize compound growth

- Invest consistently regardless of market conditions

- Keep fees below 0.5% annually

- Rebalance portfolio annually

- Avoid emotional decisions based on market volatility

According to Morningstar research, consistent investors who practice strong personal finance management average 8-10% annual returns over 20+ years.

6. Track Your Net Worth for Better Personal Finance Management

Monitoring net worth provides a comprehensive view of your personal finance management progress. Calculate by subtracting total liabilities from total assets.

How to Track Net Worth:

- Use apps like Personal Capital or Mint

- Update monthly or quarterly

- Track trends over time, not month-to-month fluctuations

- Include all assets (retirement accounts, home equity, investments)

- Subtract all debts (mortgages, student loans, credit cards)

Tracking net worth helps you see the big picture of your personal finance management efforts.

7. Optimize Taxes in Your Personal Finance Management Strategy

Tax optimization maximizes your personal finance management efficiency. Smart tax planning can save thousands annually.

Tax Optimization Strategies:

- Maximize contributions to tax-advantaged accounts (401k, IRA, HSA)

- Harvest tax losses in taxable investment accounts

- Time capital gains strategically

- Claim all eligible deductions using TurboTax or H&R Block

- Consider consulting a CPA for complex situations

The IRS website offers free resources for tax planning and personal finance management.

8. Protect Your Personal Finance Management with Insurance

Adequate insurance protects your personal finance management progress from catastrophic losses.

Essential Insurance Coverage:

- Health insurance for medical expenses

- Life insurance if others depend on your income

- Disability insurance to replace lost income

- Homeowners or renters insurance for property protection

- Auto insurance as legally required

Compare policies using Policygenius or The Zebra to find the best rates.

9. Set SMART Goals for Personal Finance Management Success

Goal setting drives personal finance management achievement. Use the SMART framework: Specific, Measurable, Achievable, Relevant, Time-bound.

Example SMART Financial Goals:

- Save $10,000 emergency fund in 12 months ($834/month)

- Pay off $5,000 credit card debt in 18 months ($278/month)

- Invest $500 monthly in retirement accounts

- Increase net worth by $20,000 this year

Break large goals into monthly milestones to maintain motivation in your personal finance management journey.

10. Continuously Educate Yourself About Personal Finance Management

Financial literacy strengthens your personal finance management capabilities. Ongoing education helps you adapt to changing economic conditions.

Top Resources for Personal Finance Management Education:

- Books: “The Total Money Makeover” by Dave Ramsey, “I Will Teach You to Be Rich” by Ramit Sethi

- Podcasts: “The Dave Ramsey Show,” “ChooseFI,” “BiggerPockets Money”

- Websites: NerdWallet, The Balance, Investopedia

- YouTube channels: Graham Stephan, The Financial Diet, Minority Mindset

- Online courses through Coursera and Udemy

Common Personal Finance Management Mistakes to Avoid

Even with good intentions, many people make preventable personal finance management errors that derail financial progress.

Top Mistakes in Personal Finance Management:

Lifestyle inflation occurs when spending increases proportionally with income, preventing wealth accumulation. Combat this by saving raises and bonuses rather than upgrading your lifestyle.

Neglecting retirement savings in your 20s and 30s costs decades of compound growth. Even small contributions early make massive differences through personal finance management discipline.

Lack of financial education leads to poor money decisions. Invest time learning personal finance management fundamentals through resources mentioned above.

Emotional spending triggered by stress or boredom derails budgets. Identify triggers and develop healthier coping mechanisms.

Failing to review finances regularly causes drift from goals. Schedule monthly personal finance management reviews to stay on track.

Best Personal Finance Management Tools and Apps

Technology simplifies personal finance management through automation and tracking.

Top Apps for Personal Finance Management:

Mint offers comprehensive budgeting with automatic transaction categorization and bill tracking.

YNAB (You Need A Budget) teaches zero-based budgeting with real-time expense tracking.

Personal Capital provides investment tracking, retirement planning, and net worth monitoring.

Acorns automatically invests spare change from purchases into diversified portfolios.

PocketGuard shows exactly how much disposable income you have after bills and goals.

Personal Finance Management for Different Life Stages

Your personal finance management priorities evolve throughout life.

Personal Finance Management in Your 20s:

- Build good money habits and credit history

- Eliminate student debt aggressively

- Start retirement savings immediately

- Focus on income growth through career development

Personal Finance Management in Your 30s:

- Maximize retirement contributions

- Save for home down payment

- Establish 529 college funds for children

- Increase emergency fund to six months

Personal Finance Management in Your 40s:

- Accelerate retirement savings

- Review and update insurance coverage

- Plan for college expenses

- Consider estate planning basics

Personal Finance Management in Your 50s+:

- Maximize catch-up retirement contributions

- Develop retirement income strategy

- Pay off mortgage if possible

- Plan healthcare and long-term care needs

Creating Your Personal Finance Management Action Plan

Transform knowledge into action with a structured personal finance management plan.

Your 30-Day Personal Finance Management Action Plan:

Week 1: Assess current finances—calculate net worth, list all debts, review income and expenses.

Week 2: Create your budget using the 50/30/20 rule, set up tracking systems, automate bill payments.

Week 3: Open emergency savings account, set up automatic transfers, research debt consolidation if needed.

Week 4: Start retirement contributions, schedule monthly financial reviews, identify one financial goal to pursue.

This structured approach makes personal finance management achievable rather than overwhelming.

Conclusion: Your Personal Finance Management Journey Starts Today

Mastering personal finance management is a lifelong journey that requires commitment, education, and consistent action. By implementing these ten proven strategies, you’ll build a strong financial foundation, achieve your goals, and create lasting financial security.

Remember that successful personal finance management isn’t about perfection—it’s about progress. Start where you are, use the resources provided, and take action today toward the financial future you deserve.

Your personal finance management transformation begins with a single step. Which strategy will you implement first?

For more resources on personal finance management, explore our related articles on budgeting basics, investment strategies, and debt elimination methods.

FAQ: Personal Finance Management

What is personal finance management? Personal finance management is the process of budgeting, saving, investing, and planning your money to achieve financial goals and security.

How do I start personal finance management? Begin with tracking expenses for 30 days, creating a budget, opening a savings account, and setting one specific financial goal.

What percentage should I save for personal finance management? Aim to save at least 20% of gross income for retirement, emergency funds, and other financial goals.

Which personal finance management app is best? Mint and YNAB are top choices—Mint for automated tracking, YNAB for hands-on budgeting discipline.

How much emergency fund do I need in personal finance management? Save three to six months of living expenses in an accessible savings account for financial emergencies.