Introduction

If you’re confused about the new money rules in India for 2026, you’re not alone. Millions of Indians are trying to understand how recent tax changes, banking fee revisions, and credit card reward adjustments will impact their daily spending and savings.

The good news? Income up to ₹12 lakh is now tax-free under the new regime, thanks to changes announced in Budget 2025. But that’s just the beginning. From credit card fees to emergency fund requirements in an inflation-adjusted world, this comprehensive guide breaks down everything you need to know to make smart money decisions in 2026.

What Changed from January 1, 2026?

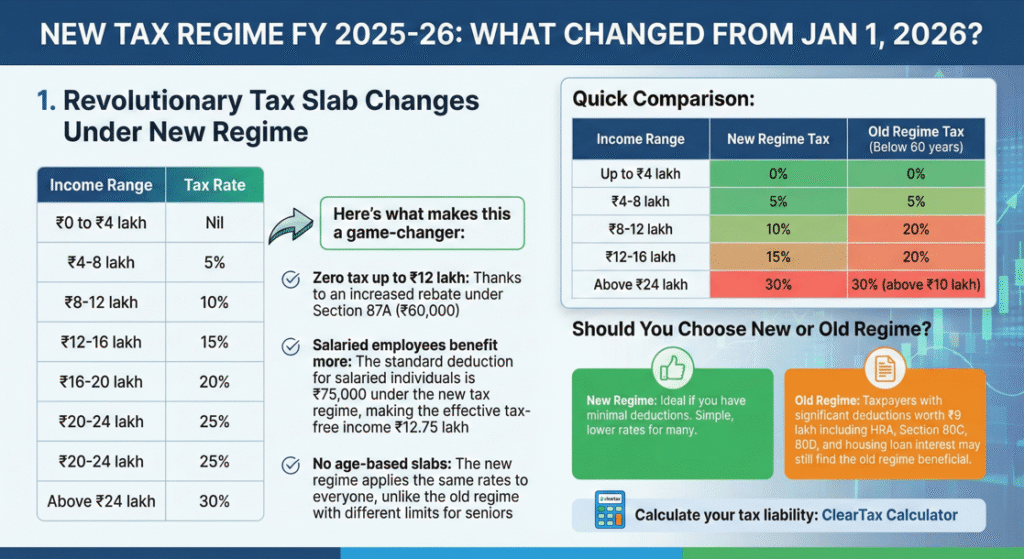

1. Revolutionary Tax Slab Changes Under New Regime

The new tax regime tax slabs for FY 2025-26 are structured as follows: ₹0 to ₹4 lakh is taxed at nil, ₹4-8 lakh at 5%, ₹8-12 lakh at 10%, ₹12-16 lakh at 15%, ₹16-20 lakh at 20%, ₹20-24 lakh at 25%, and income above ₹24 lakh at 30%.

Here’s what makes this a game-changer:

Key Highlights:

- Zero tax up to ₹12 lakh: Thanks to an increased rebate under Section 87A (₹60,000)

- Salaried employees benefit more: The standard deduction for salaried individuals is ₹75,000 under the new tax regime, making the effective tax-free income ₹12.75 lakh

- No age-based slabs: The new regime applies the same rates to everyone, unlike the old regime with different limits for seniors

Quick Comparison:

| Income Range | New Regime Tax | Old Regime Tax (Below 60 years) |

|---|---|---|

| Up to ₹4 lakh | 0% | 0% |

| ₹4-8 lakh | 5% | 5% |

| ₹8-12 lakh | 10% | 20% |

| ₹12-16 lakh | 15% | 20% |

| Above ₹24 lakh | 30% | 30% (above ₹10 lakh) |

Should You Choose New or Old Regime?

The new regime is ideal if you have minimal deductions. However, taxpayers with significant deductions worth ₹9 lakh including HRA, Section 80C, 80D, and housing loan interest may still find the old regime beneficial.

Calculate your tax liability: ClearTax Calculator

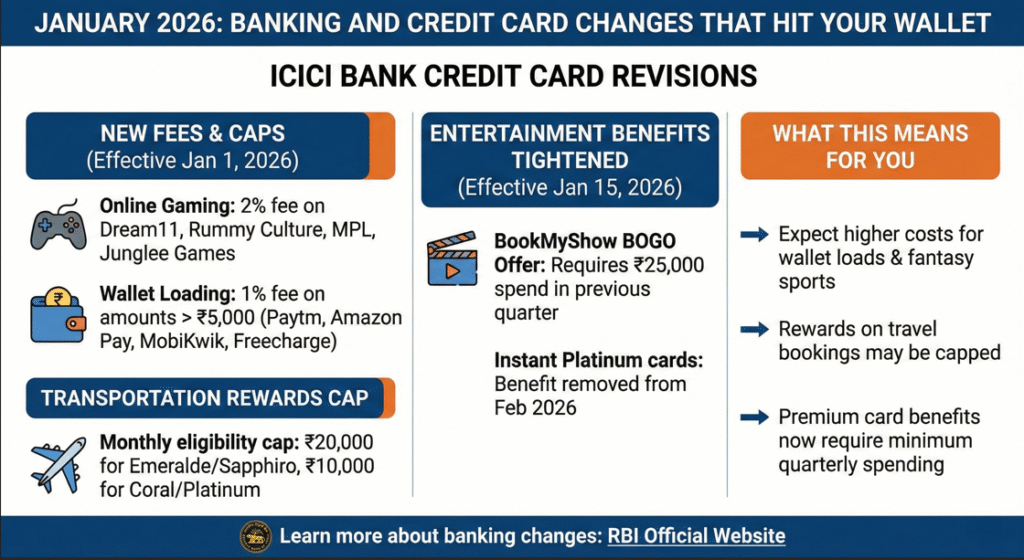

2. Banking and Credit Card Changes That Hit Your Wallet

January 2026 brought significant changes to how banks charge fees and distribute rewards. Here’s what you need to know:

ICICI Bank Credit Card Revisions

Starting January 2026, ICICI Bank will levy a 2% transaction fee on online gaming platforms and a 1% charge on wallet loads of ₹5,000 or more to third-party wallets like Paytm and Amazon Pay.

New Fees Effective from January 15, 2026:

- Online Gaming: 2% fee on Dream11, Rummy Culture, MPL, Junglee Games

- Wallet Loading: 1% fee on amounts exceeding ₹5,000 (Paytm, Amazon Pay, MobiKwik, Freecharge)

- Transportation: Monthly reward eligibility is capped at ₹20,000 for premium cards like Emeralde and Sapphiro, and ₹10,000 for mid-tier cards like Coral and Platinum

Entertainment Benefits Tightened: Cardholders must spend ₹25,000 in the previous calendar quarter to access BookMyShow Buy-One-Get-One offers, while Instant Platinum cards lose this benefit entirely from February 2026.

What This Means for You:

- If you frequently load wallets or play fantasy sports, expect higher costs

- Your credit card rewards on travel bookings may be capped

- Premium card benefits now require minimum quarterly spending

Learn more about banking changes: RBI Official Website

7 New Money Rules From January 1, 2026

January 2026 marks a watershed moment for Indian personal finance. Here are the seven critical money rules that took effect and how they impact your wallet:

Rule #1: Revolutionary Tax Slabs Under New Regime

What Changed: The new tax regime now offers zero tax on income up to ₹12 lakh (including standard deduction of ₹75,000 for salaried employees).

Who Benefits: Salaried employees earning ₹8-15 lakh annually with minimal deductions.

Action Required:

- Calculate tax under both old and new regimes

- File Form 12BB with your employer if opting for old regime

- The new regime is now the default

See detailed tax slab table in the next section

Rule #2: PAN-Aadhaar Linking Now Mandatory (Deadline Passed!)

What Changed: Individuals who failed to connect their PAN with Aadhaar by December 31, 2025 now have inoperative PANs from January 1, 2026.

Critical Impact:

- ❌ Cannot file income tax returns

- ❌ Higher TDS/TCS rates (20% instead of applicable rates)

- ❌ Cannot open new bank accounts or update KYC

- ❌ Blocked from investing in mutual funds, stocks

- ❌ Loan applications rejected

How to Reactivate:

- Pay ₹1,000 penalty through e-Pay Tax on Income Tax portal

- Complete PAN-Aadhaar linking online at incometax.gov.in

- Wait 7-30 days for reactivation

Exemptions: NRIs, non-citizens, individuals 80+, residents of Assam, Meghalaya, J&K, and Ladakh

Learn more: Income Tax Department – Link Aadhaar

Rule #3: UPI Transaction Limits Increased for Specific Categories

What Changed: NPCI raised UPI transaction limits effective from September 15, 2025 (continuing into 2026):

New UPI Limits:

| Category | Per Transaction | Per Day |

|---|---|---|

| Person-to-Person (P2P) | ₹1 lakh | ₹1 lakh |

| Insurance & Investments | ₹5 lakh (previously ₹2 lakh) | ₹10 lakh |

| Travel & Collections | ₹5 lakh | ₹10 lakh |

| Credit Card Bills | ₹5 lakh | ₹6 lakh |

| Government e-Marketplace (GeM) | ₹5 lakh (previously ₹1 lakh) | ₹10 lakh |

| Education | ₹5 lakh | ₹10 lakh |

| New UPI Registration | ₹5,000 | ₹5,000 (first 24 hours) |

Additional UPI Rules from August 2026:

- Balance check limited to 50 times per day per app

- Auto-balance display after every transaction

- Maximum 25 bank account linkings per day

- Pending transaction status checks: 3 times per transaction (90-second gap)

What This Means: ✅ Higher convenience for large insurance premium payments

✅ Easy mutual fund SIP transactions without bank transfers

✅ Simplified education fee payments

⚠️ First-time UPI users face ₹5,000 daily limit for 24 hours (security measure)

Official source: NPCI UPI Circulars

Rule #4: Credit Score Updates Now Bi-Monthly (Every 15 Days)

What Changed: RBI mandated that banks and NBFCs report credit data to CIBIL and other bureaus five times per month instead of monthly—on the 7th, 14th, 21st, 28th, and month-end.

Major Impact:

- ✅ Faster Improvements: Timely EMI payments reflect within 15 days instead of 30-45 days

- ✅ Quicker Error Resolution: Disputes must be resolved within 30 days (with ₹100/day penalty after that)

- ✅ Free Annual Report: One free credit report per year from each bureau

- ⚠️ Faster Penalties: Late payments also reflect faster—even 1-day delay impacts score within a week

New Borrower Rights:

- Lenders must notify you via SMS/email when your credit report is accessed

- Banks must warn customers before reporting defaults

- Clear explanations required for loan rejections

Practical Example: If you pay your credit card bill on January 5, your improved utilization ratio could reflect by January 14-15 instead of waiting until February.

Action Steps: ✅ Set payment reminders 2-3 days before due dates

✅ Check free credit report annually from CIBIL

✅ Maintain credit utilization below 30%

✅ Dispute errors immediately—resolution now mandatory within 30 days

Learn more: RBI Master Direction on Credit Information Reporting

Rule #5: Zero Foreclosure Charges on Floating-Rate Loans

What Changed: RBI banned prepayment and foreclosure charges on all floating-rate loans sanctioned or renewed from January 1, 2026.

Who Benefits: ✅ Home Loan Borrowers: No charge for early closure or part-prepayment

✅ Personal Loan Holders: Pay off floating-rate personal loans anytime

✅ Car Loan Borrowers: If your car loan is floating-rate (check loan agreement)

✅ MSME Borrowers: Small business loans up to ₹50 lakh from certain lenders

What’s Covered:

- All floating-rate loans to individuals for non-business purposes (any amount)

- Business loans from commercial banks, Tier 1/2 NBFCs, All India Financial Institutions

- Loans up to ₹50 lakh from Small Finance Banks, Regional Rural Banks, Tier 3 cooperative banks, NBFC-ML

What’s NOT Covered: ❌ Fixed-rate loans (foreclosure charges may still apply—typically 2-6%)

❌ Loans sanctioned before January 1, 2026 (check your agreement)

❌ Foreign currency loans

❌ Export credit

How to Benefit:

- Check your loan agreement—confirm it’s floating rate

- Request prepayment/foreclosure from your lender (no lock-in period!)

- Verify zero charges in your Key Facts Statement (KFS)

- Calculate interest savings vs. keeping funds invested

Example: If you have a ₹30 lakh home loan at 8.5% with 15 years remaining, prepaying ₹5 lakh saves approximately ₹6.5 lakh in interest—with zero penalty from 2026 onwards!

Official source: RBI Pre-payment Charges on Loans Directions, 2025

Rule #6: Credit Card Fee Changes and Reward Caps

What Changed: Major banks (especially ICICI Bank) introduced new fees and reward restrictions from January 2026.

ICICI Bank Changes (Effective January 15, 2026):

New Fees:

- Online Gaming Platforms: 2% fee on Dream11, Rummy Culture, MPL, Junglee Games

- Wallet Loading: 1% fee on amounts exceeding ₹5,000 to third-party wallets (Paytm, Amazon Pay, MobiKwik, Freecharge)

Reward Caps:

- Monthly reward cap on transportation: ₹20,000 for premium cards (Emeralde, Sapphiro), ₹10,000 for mid-tier (Coral, Platinum)

- BookMyShow BOGO: Requires ₹25,000 quarterly spend

- Instant Platinum cards lose entertainment benefits from February 2026

What This Means: ⚠️ Loading ₹10,000 to Paytm now costs ₹100 extra

⚠️ ₹1,000 gaming transaction incurs ₹20 fee

⚠️ Transportation rewards limited even for premium cardholders

Smart Strategies: ✅ Use direct bank transfers for wallet loads (avoid 1% fee)

✅ Review quarterly spending to maintain benefits

✅ Compare cards if your usage patterns don’t fit new rules

✅ Consider debit cards for gaming/wallet transactions (no fee)

Source: ICICI Bank Credit Card Changes 2026

Rule #7: Stricter Dormant Bank Account Monitoring

What Changed: RBI tightened monitoring of dormant/inactive bank accounts to prevent fraud and money laundering.

Definition: A bank account becomes “dormant” if there are no customer-initiated transactions for 2 years (24 months).

New Compliance Requirements:

- Banks must notify customers via SMS/email before marking accounts dormant

- Regular KYC updates mandatory for reactivation

- Enhanced due diligence for accounts with suspicious patterns

- Accounts with pending KYC may be frozen

How to Keep Accounts Active: ✅ At least one transaction per year (withdrawal, deposit, online transfer)

✅ Update KYC details every 2 years

✅ Respond to bank notifications promptly

✅ Link mobile number and email for alerts

Reactivation Process:

- Visit home branch with ID proof and PAN card

- Submit KYC documents

- Complete verification (may take 3-5 working days)

- Account reactivated with transaction limits restored

Why This Matters: Dormant accounts are used for fraud, tax evasion, and money laundering. The stricter rules protect genuine customers while preventing financial crimes.

Learn more: RBI – Know Your Customer Guidelines

Step-by-Step 2026 Money Plan for Indians

Step 1: Understand Your Salary and Tax Slab

For Salaried Employees (₹8-12 Lakh Income):

Let’s say you earn ₹10 lakh annually. Under the new regime:

- Gross Income: ₹10,00,000

- Less: Standard Deduction: ₹75,000

- Taxable Income: ₹9,25,000

- Tax Calculation:

- First ₹4 lakh: ₹0

- Next ₹4 lakh (₹4-8 lakh): ₹20,000 (5%)

- Remaining ₹1.25 lakh: ₹12,500 (10%)

- Total Tax: ₹32,500

- After rebate: ₹0 (since taxable income is below ₹12 lakh)

Action Items: ✅ Use online tax calculators to estimate your exact liability

✅ Compare both regimes if you have significant deductions

✅ Update your Form 12BB with your employer

Calculate your tax: Bajaj Finserv Tax Calculator

Step 2: Adjust Your Budget Using the 50-30-20 Rule

With potentially lower tax outgo, you’ll have extra savings. Here’s how to allocate wisely:

The Modified 50-30-20 Rule for 2026:

- 50% – Essentials: Rent, groceries, utilities, EMIs, insurance

- 30% – Lifestyle: Dining out, entertainment, hobbies (watch for new credit card fees!)

- 20% – Savings & Investments: Emergency fund, retirement, goals

Example Budget for ₹8 Lakh Annual Income (₹66,666/month):

- Essentials: ₹33,333

- Lifestyle: ₹20,000

- Savings: ₹13,333

Tax Savings Opportunity:

If you save ₹30,000 in taxes due to new slabs, add this directly to your emergency fund or investments. Don’t let lifestyle inflation eat it up!

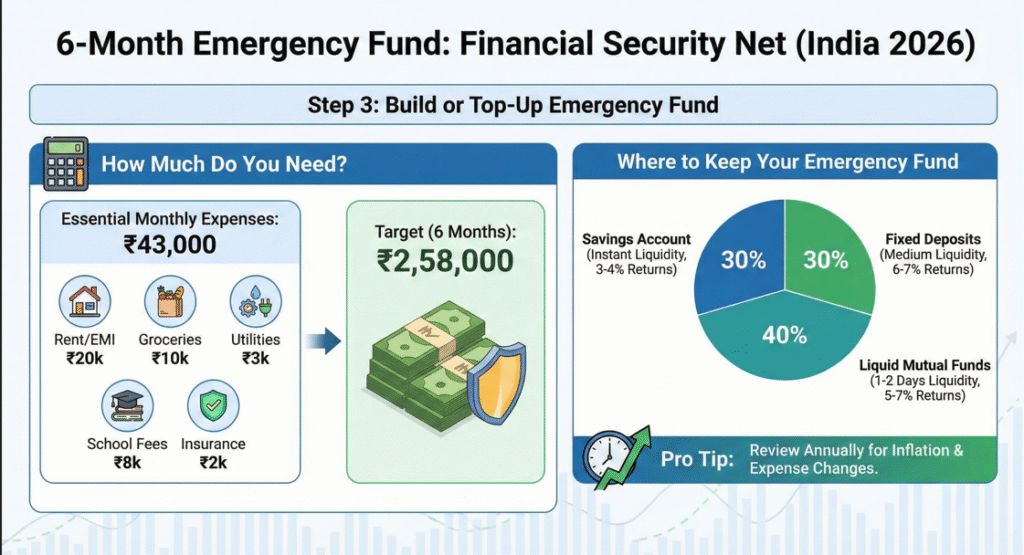

Step 3: Build or Top-Up Emergency Fund for 6 Months

The general guideline is to maintain 3-12 months of essential household expenses, with married individuals with children recommended to save 6 months.

How Much Do You Need in 2026?

Essential costs like healthcare, food, and fuel have significantly increased in 2025, meaning if you had ₹3 lakh set aside in 2022, you may now require ₹3.5-4 lakh to maintain the same financial security.

Calculate Your Emergency Fund:

- List Essential Monthly Expenses:

- Rent/EMI: ₹20,000

- Groceries: ₹10,000

- Utilities: ₹3,000

- School fees: ₹8,000

- Insurance: ₹2,000

- Total: ₹43,000

- Multiply by 6 months: ₹43,000 × 6 = ₹2,58,000

Where to Keep Your Emergency Fund:

A smart mix includes 30% in savings accounts, 30% in fixed deposits, and 40% in liquid funds for both liquidity and inflation-beating returns.

| Option | Returns | Liquidity | Best For |

|---|---|---|---|

| Savings Account | 3-4% | Instant | 1-2 months expenses |

| Fixed Deposit | 6-7% | Medium (premature withdrawal) | 2-3 months expenses |

| Liquid Mutual Funds | 5-7% | 1-2 days | Remaining amount |

Pro Tip: Review your emergency fund once a year to ensure it covers 3 to 6 months of essential expenses, accounting for inflation.

Learn more: Emergency Fund Calculator

Step 4: Decide Where to Invest Extra Money

Now that your emergency fund is sorted and you’re saving on taxes, here’s where to invest:

Short-Term Goals (1-3 years):

- Debt mutual funds

- Fixed deposits

- Recurring deposits

Medium-Term Goals (3-5 years):

- Balanced mutual funds

- Public Provident Fund (PPF)

- National Pension System (NPS)

Long-Term Goals (5+ years):

- Equity mutual funds (index funds, ELSS)

- Employee Provident Fund (EPF)

- Direct equity (if you understand stocks)

Tax-Saving Investments (Under Old Regime Only):

- Section 80C: EPF, PPF, ELSS, life insurance (up to ₹1.5 lakh)

- Section 80D: Health insurance premiums

- Section 80CCD(1B): Additional NPS contribution (₹50,000)

Sample Investment Strategy for ₹10 Lakh Income:

- Emergency Fund (completed): ₹2.5 lakh

- PPF/EPF: ₹1.5 lakh/year

- ELSS/Index Funds SIP: ₹10,000/month (₹1.2 lakh/year)

- Health Insurance: ₹25,000/year

- Term Insurance: ₹15,000/year

Investment resources: SEBI Investor Education

Common Mistakes Indians Will Make in 2026

Mistake #1: Not Using New Tax Slab Benefits

Many salaried employees earning ₹8-12 lakh will continue using the old regime by default, not realizing fewer than 20% of taxpayers remain in the old tax regime.

Solution: Calculate tax under both regimes every year. The new regime is default; you need to actively opt for old regime if beneficial.

Mistake #2: Overspending Because EMIs/Interest Got Cheaper

Lower taxes don’t mean higher spending capacity! RBI’s inflation projections suggest consumer inflation could be around 4-4.5% in 2026.

Solution: Stick to your 50-30-20 budget. Redirect tax savings to investments, not lifestyle upgrades.

Mistake #3: Ignoring Credit Card Fee Changes

Continuing to use credit cards for wallet loads and gaming without factoring in the new 1-2% fees can significantly reduce reward value.

Solution: Review your credit card usage patterns. Consider direct bank transfers for wallet loads to avoid fees.

Mistake #4: Not Adjusting Emergency Fund for Inflation

Healthcare costs in India are rising at 14% annually, far outpacing general inflation.

Solution: Increase your emergency fund by 5-7% annually to keep pace with rising expenses.

Mistake #5: Confusing Tax-Free Income with No Tax Planning

Just because income up to ₹12 lakh is tax-free doesn’t mean you shouldn’t plan for retirement, insurance, and long-term goals.

Solution: Continue systematic investing regardless of your current tax liability.

Simple Checklist / FAQ

What should a salaried person with ₹8-12 lakh income do in 2026?

Immediate Actions: ✅ Verify you’re on the new tax regime (it’s default)

✅ Calculate exact tax savings compared to 2025

✅ Review credit card fees and adjust spending patterns

✅ Check if emergency fund covers 6 months expenses

✅ Start/continue SIP in equity mutual funds (₹5,000-10,000/month)

✅ Ensure adequate health insurance (minimum ₹10 lakh cover)

✅ Buy term insurance if you have dependents (₹1 crore cover)

How much emergency fund in 2026 accounting for inflation?

Salaried employees need 6 months of emergency funds, while business owners and freelancers need 9-12 months due to income variability.

Updated Formula for 2026:

- Calculate monthly essential expenses

- Multiply by 6 (or 9-12 for entrepreneurs)

- Add 5-7% buffer for annual inflation

- Review and top-up every year

Example: If you needed ₹3 lakh in 2024, you need approximately ₹3.2-3.3 lakh in 2026.

Which financial goals to plan first?

Priority Order:

- Adequate Insurance: Health (₹10-15 lakh) + Term (10x annual income)

- Emergency Fund: 6 months expenses in liquid form

- Retirement Planning: Start NPS/PPF/equity mutual funds

- Children’s Education: Child education plans or dedicated SIPs

- Home Purchase: Down payment fund (separate from emergency fund)

- Wealth Creation: Aggressive equity investments

Should I switch to old tax regime?

Switch to OLD regime if:

- You claim HRA (living in rented accommodation)

- Home loan interest > ₹2 lakh/year

- Total deductions under 80C, 80D, 80CCD exceed ₹2 lakh

- You have dependent parents and claim medical expenses

Stick to NEW regime if:

- Total deductions < ₹1.5 lakh

- You don’t claim HRA

- You prefer simpler tax filing

- Your income is between ₹8-15 lakh with minimal investments

How to save more with new tax slabs?

Smart Strategies:

- Maximize standard deduction: Ensure employer deducts the full ₹75,000

- Optimize salary structure: Ask for more basic pay, less allowances (under new regime)

- Use employer NPS contribution: Section 80CCD(2) deduction available in both regimes (up to 10% of basic)

- Claim family pension deduction: Up to ₹15,000 (if applicable)

- Invest tax savings: Don’t spend the saved amount, invest it for compounding

Conclusion: Your 2026 Action Plan

The changes in 2026 present a genuine opportunity for middle-class Indians to save more and invest smarter. Here’s your action roadmap:

This Month:

- Calculate your tax liability under both regimes

- Review all credit card statements for new fees

- Calculate required emergency fund amount

This Quarter:

- Build/top-up emergency fund to target amount

- Start SIPs if not already investing

- Review and update insurance coverage

This Year:

- Maximize tax-saving investments (if using old regime)

- Track credit card rewards vs. fees quarterly

- Increase emergency fund by 5-7% for inflation

- Review and rebalance investments twice yearly

Remember: Income up to ₹12 lakhs is tax-free under the new regime, but smart financial planning goes beyond just taxes. Build your emergency fund, invest systematically, maintain adequate insurance, and review your finances at least once a quarter.

Additional Resources

Official Government Links:

- Income Tax Department

- National Securities Depository Limited

- Reserve Bank of India

- Securities and Exchange Board of India

Tax Calculators:

Financial Planning Tools:

Banking Updates:

Disclaimer: This article is for informational purposes only and should not be considered financial advice. Tax laws and banking regulations can change. Please consult a certified financial planner or tax advisor for personalized guidance based on your specific situation.

Last Updated: January 15, 2026